HOPES that the Island’s cooling property market could open up opportunities for would-be homeowners appear to have been dashed by higher mortgage repayment rates, according to “worrying” new statistics.

But industry representatives have said that affordability “will come back” subject to possible drops in the Bank of England base rate, which was recently held at 5.25%.

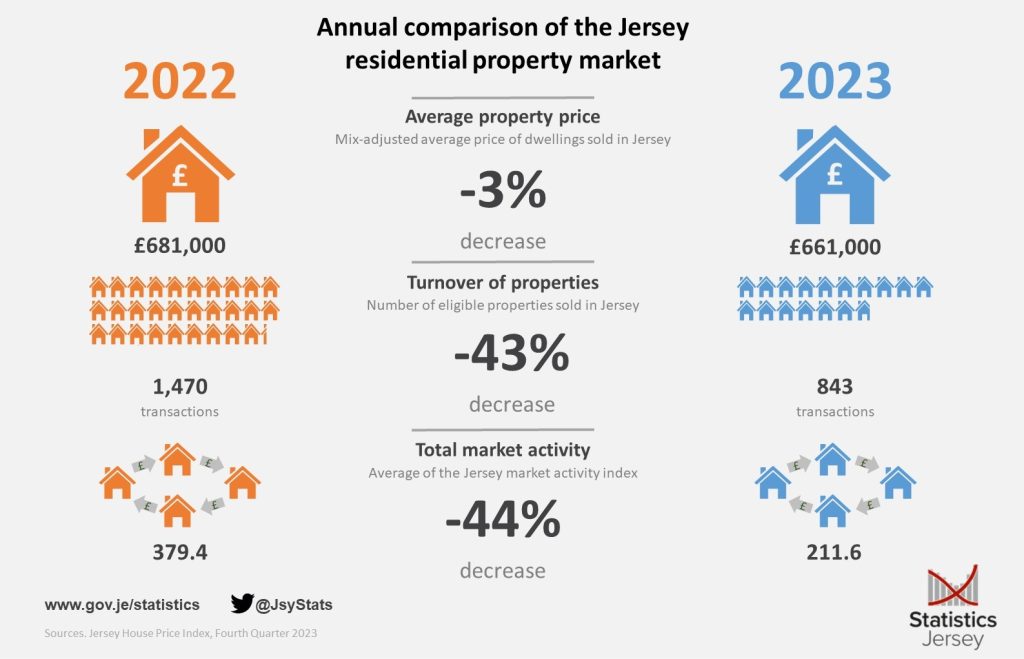

Figures released yesterday by Statistics Jersey, detailing the latest House Price Index, showed that 2023 saw the second biggest annual drop in property prices since at least 1986.

However, the accompanying report stated that housing was “significantly less affordable” last year than in 2022, due to an increase in interest rates.

Key figures

In the final quarter of 2023, the average cost of a home in Jersey stood at £636,000 – down from the figure of £681,000 recorded in the previous quarter.

Overall, the average price of a home in the Island last year was 3% lower than in 2022. This was the first annual decrease in price since 2013.

Advertised private-sector rental prices were also slightly lower than the year before.

The major slump in property sales seen towards the end of last year eased slightly in the final quarter – thanks to the sale of newly built units – but the overall turnover of properties for 2023 (843) was 43% lower than it was in 2022.

It was also the lowest annual turnover for at least two decades, partly driven by three- and four-bedroom houses – where sales for both were down by 55%.

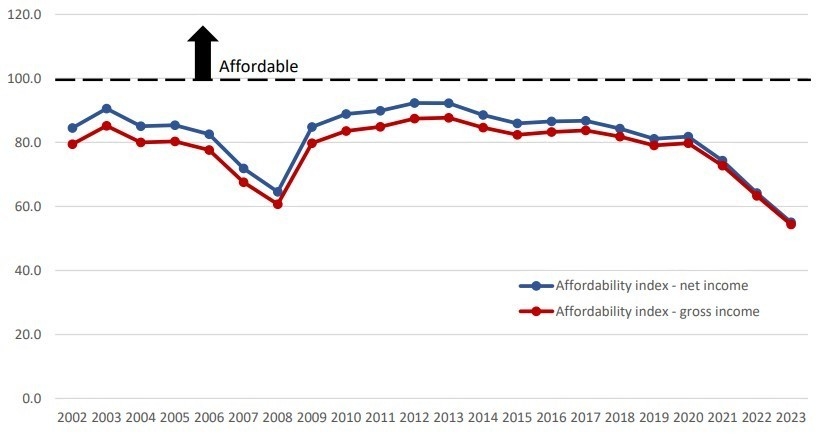

The ratio of average prices against household income in Jersey was lower than it was in 2022 for all property types.

However, the report noted that this was “outweighed by higher mortgage interest costs”, resulting in worse housing affordability overall.

The issue of increased mortgage rates came to the fore earlier this year, when Jersey Consumer Council chair Carl Walker questioned why some Island homeowners were paying hundreds of pounds more in repayments compared to UK borrowers who used the same bank.

“Overall, housing was significantly less affordable in 2023 compared with 2022, due to the increase in interest rates. This is despite the increase in household income – based on the change in average earnings – being 7.7% and property prices decreasing by around 3%,” the report explained.

It stated that a working household with an average income was able to “service a mortgage affordably” on the purchase of a median-priced one-bedroom flat – but could not do so with “a median-priced house of any size or a two-bedroom flat”.

The view from industry insiders

Broadlands director Harry Trower – who last year warned that transactions had “fallen off a cliff” – said the “worrying” statistics reflected an “affordability crisis” caused by relatively high interest rates and property prices.

“The fact that average earners cannot afford anything over a median-priced one-bedroom apartment makes poor reading.

“The Housing Minister should be looking at affordability,” he continued.

“Some people can’t even look at the available properties because they can’t pass the banks’ stress tests.”

However, Mr Trower said it was “important to remember” that the statistics reflected the market’s performance at the end of last year – not the current situation.

“What is happening is that there has been an increase in market activity since January, because the base rate held level,” he added.

“[This year] will hopefully have drops in the base rate and affordability will come back. We will likely see a drop in property prices to reflect this, but it will not be catastrophic.

“It will drop to reflect the new affordability on mortgages. This will not be a sudden drop but will happen overtime as rates ease – hopefully.”

Peter Seymour, of the Mortgage Shop, stressed that the issue was not solely related to interest rates, as prices still “have to fall”.

“House prices will continue to fall as vendors find they can’t sell,” he continued, although he echoed Mr Trower’s comments about increased market activity so far this year.

“The market is already starting to move – certainly any reduction in rates will help to stimulate it.”

Chief Minister Lyndon Farnham said: “Increasing home ownership for Islanders – especially young people and families – as well as providing better opportunities within the rental market, is a high priority for this government.”

He added: “The high cost of borrowing is a concern and I have discussed the matter with Deputy Ian Gorst, who will be speaking to the Jersey Bankers Association with a view to encouraging banks and local lenders to introduce more competitive rates – as we are seeing in the UK.”