Sponsored Content

DURING the week Wall Street succumbed to nervousness with major technology names struggling amid President Trump’s tariff threats.

Confusing jobs data last Friday added to market woes, as the monthly payroll number came in lower than expected. However, there were upward revisions to the previous two months indicating that the three-month average was still looking extremely healthy, showing little sign of an immediate jobs’ slowdown.

The corresponding unemployment rate surprisingly fell to just 4% and hourly wage rates rose more than expected, leaving analysts wrestling with what it all means.

What we do know is that the Federal Reserve is watching carefully for a “cooling off” of the jobs market, which would be a cue for them to consider cutting interest rates. Adding yet more uncertainty was the latest University of Michigan survey. This showed Americans believe that future inflation will be higher under Trump’s economic policies, dampening overall consumer confidence. In reality, the next Federal committee meeting is not until 18/19 March, so there is a great deal more Trump rhetoric to flow under the bridge before the next rate decision, including his weekend pronouncement that he is serious about Canada becoming the 51st state in America.

President Trump continues to successfully use the weight of the US to impose itself on the rest of the world. This was particularly so with his announcement that he is now threatening reciprocal tariffs. Nowhere is this more evident than in Europe where a 10% tariff is applied for imported US cars. Suddenly, the head of the European Trade Committee is suggesting that this may be reduced to the equivalent of 2.5%, thus matching the US tariff on European cars.

Closer to home, the UK is struggling under combined political and economic problems, with the Bank of England now forecasting a significant cut to growth expectations this year – the prediction is for growth to rise just 0.75% in 2025, more closely resembling continental Europe.

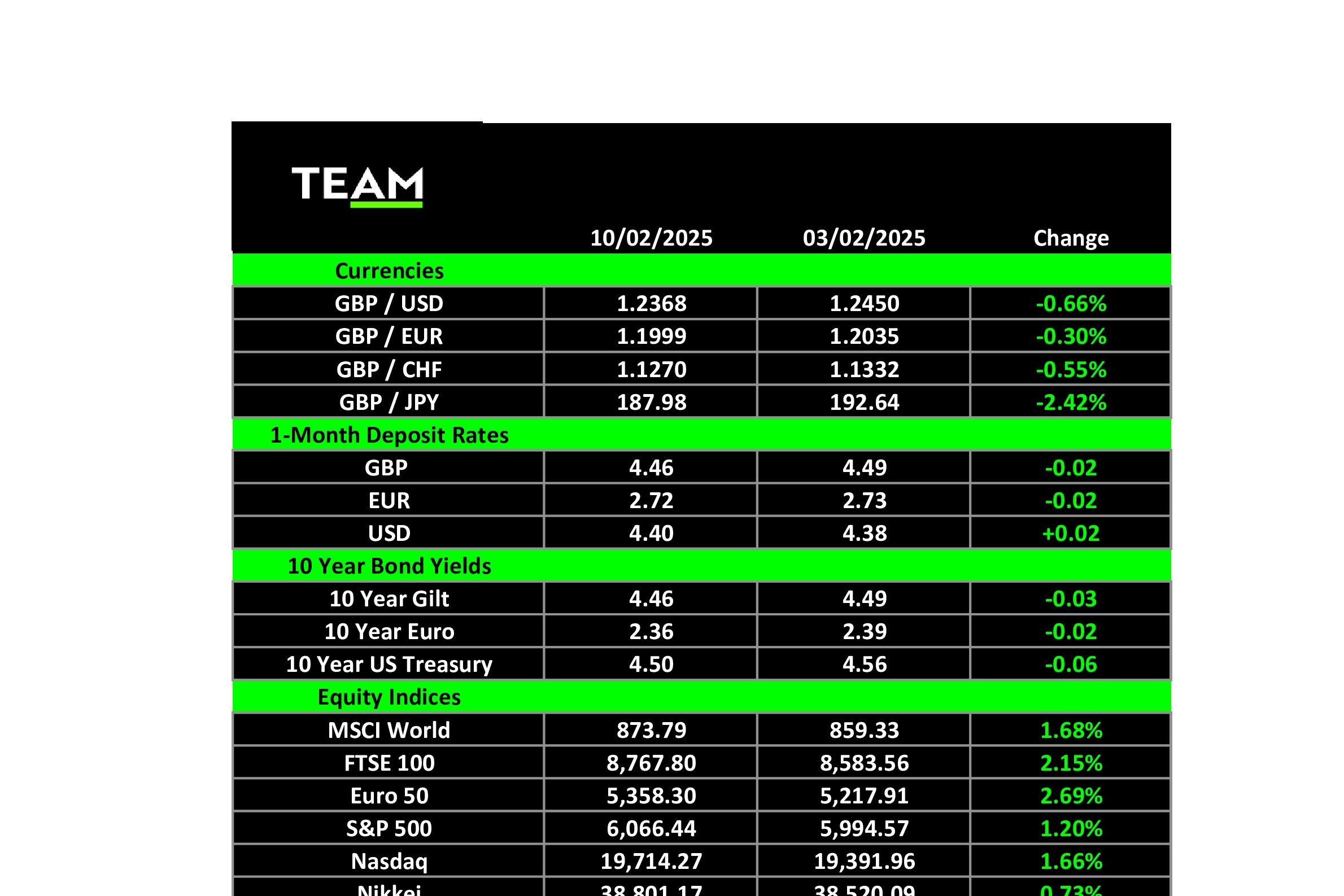

For the third time since the peak of the Bank of England’s base rate of 5.25%, the UK Monetary Policy Committee decided to cut rates by 0.25%, this time taking it to 4.5%. At the margin, this is good news, but governor Andrew Bailey cautioned about more rate cuts as his economists are still forecasting that current inflation will rise from 2.5% to 3.7% by this autumn. For those property owners expecting mortgage-rate cuts, this will depend on banks allowing their profit margins to move lower and government bond prices to rise with falling yields. So far neither are resolutely going the right way for homeowners.

Turning to individual company news, spirits producer and Guinness brewer Diageo scrapped its long-standing sales growth guidance, blaming the uncertainty over US tariffs and weak demand in its key markets as the company comes under investor pressure to improve performance. Its shares are now 45% below its December 2021 peak.

Meanwhile, arch activist shareholder Elliott has taken a sizeable stake in BP. The shares predictably rose 7% in the hope that the company underperformance against its peer group could be arrested as Elliott agitates the oil company board for change that gives rise to increased shareholder value.

News this week will evolve around Consumer Price Indices for both the US (today) and continental Europe (Friday). For the past two months, US inflation figures have proved lower than expected, providing comfort for investors. The forecast for today’s January figures is a monthly core rate of 0.3% (3.1% annualised) and headline rate of 2.9% annualised. Will investors receive a “hat trick” of good news? We will find out at around 1.30pm UK time.

As for Europe, there will more interest about producer price inflation and the preliminary estimate of Gross Domestic Product for the fourth quarter of 2024, which is also due to be announced on Friday.