Sponsored Content

Team Asset Management’s Craig Farley offers this week’s round-up of global markets

IT’S been a topsy-turvy week across global financial markets, with risk assets gyrating wildly on a bubbling-up of trade tensions sparked by US President Donald Trump and his MAGA (Make America Great Again) team.

Last week’s Deep Seek revelations prompted panic-sell activity in Nvidia and all things AI, before relative calm was restored following working theories that a) the Chinese company in question had spent hundreds of millions of dollars more on advanced semiconductor chips than initially disclosed, and b) the Deep Seek R1 model performed poorly across a range of metrics when measured against established US peers.

The sell-off in the technology sector prompted a call-to-arms from the retail investor community, who stepped in and purchased almost one trillion dollars-worth of QQQ (the Nasdaq-100 index ETF tracker), culminating in the largest weekly inflow to the product in four years. Sensible dip-buying into an established long-term investment theme, or the strong whiff of FOMO? Only time will tell…

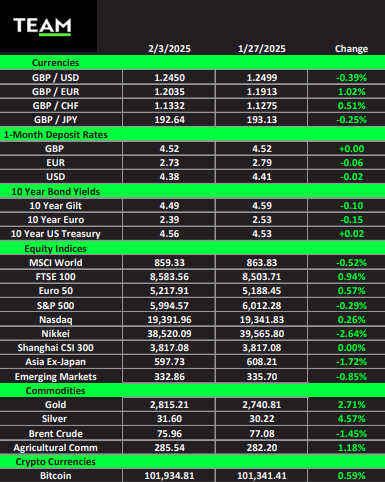

Insatiable appetite for American stocks overwhelmed the mixed macroeconomic data that was released during the week. US fourth-quarter GDP was +2.3% (versus +2.6% expected, and sharply down from the 3% run rate of the past few quarters), while Personal Consumption Expenditures (PCE) inflation was +4.2% (versus +3.2% expected). Meanwhile, the European Central Bank cut interest rates again by 25 basis points to 2.75%, with president Christine Lagarde pointing to anaemic growth as a key factor.

US major indices closed out January with strong performance, every sector in the “green” (profit), and seasoned market observer’s hopeful that the “January Barometer” will play out this year. To recap, the January Barometer, first devised by Yale Hirsch of Stock Trader’s Almanac fame, holds that a positive close for the S&P 500 Index in January portends better than average returns for US stocks for the full year.

Using S&P 500 index data going back to 1950, a positive January return has resulted in an average annual return of +16.8%. This compares to an average annual return of -1.8% if January is a negative month. Fans of seasonality work will point out that the January Barometer has registered only 12 errors between 1950 and 2025, for an accuracy ratio of 84%.

Enter “The Donald”, who, over the weekend, followed through his repeated protectionist threats by announcing a series of aggressive tariffs on America’s trading partners, including 25% on Mexico and Canada, and 10% on China. In true Trump style, the tariffs were subsequently “delayed” for a period of weeks following horse-trading with the various governments in question.

Markets have been jittery in response to the news, which came as a clear surprise to many. With Europe the next obvious target, investors are being forced to dust off their game-theory textbooks and try to make sense of the short-term and longer-term implications.

Separately, the Trump administration, specifically DOGE (Department of Government Efficiency) has wasted little time in unleashing a series of executive orders aimed at reigning in federal spending. They include an official suspension of US military aid to Ukraine, the termination of any federal employee that doesn’t show up for work in person by 6 February and the introduction of blockchain technology to track US government spending effectively.

With the motivation for the tariff measures seemingly at direct odds with likely policy outcomes, investors have, en masse, acted first, leaving questions for later. Risk assets tumbled late in the week, led by the crypto space and semiconductor stocks. The dollar surged, putting pressure on ex-US currencies and dollar debt holders. Gold was arguably the standout asset this week, breaching the $2,800 level for the first time, adding further credibility to its status as a haven asset and store of value.