Sponsored Content

Craig Farley of Team Asset Management offers this week’s global market review.

A strong gale whipped up across the financial market landscape this week, displacing the calm sailing waters of 2024 with choppy conditions, culminating in a sea of red for risk assets.

All major headline indexes including the bellwether S&P 500 large-cap, technology-laden Nasdaq, Dow Industrials and Russell 2000 (small cap) were down sharply as the lens of the market shifted its attention to worries over a second inflationary wave and the debt issue plaguing G7 economies.

Initial reports that the incoming Trump administration might take a softer stance on tariffs were quickly dispelled by “the Donald” himself through his media platform Truth Social. The result was confusion and consternation among investors, offering a good working example of the additional unpredictability that will probably accompany the president-elect’s second term in office.

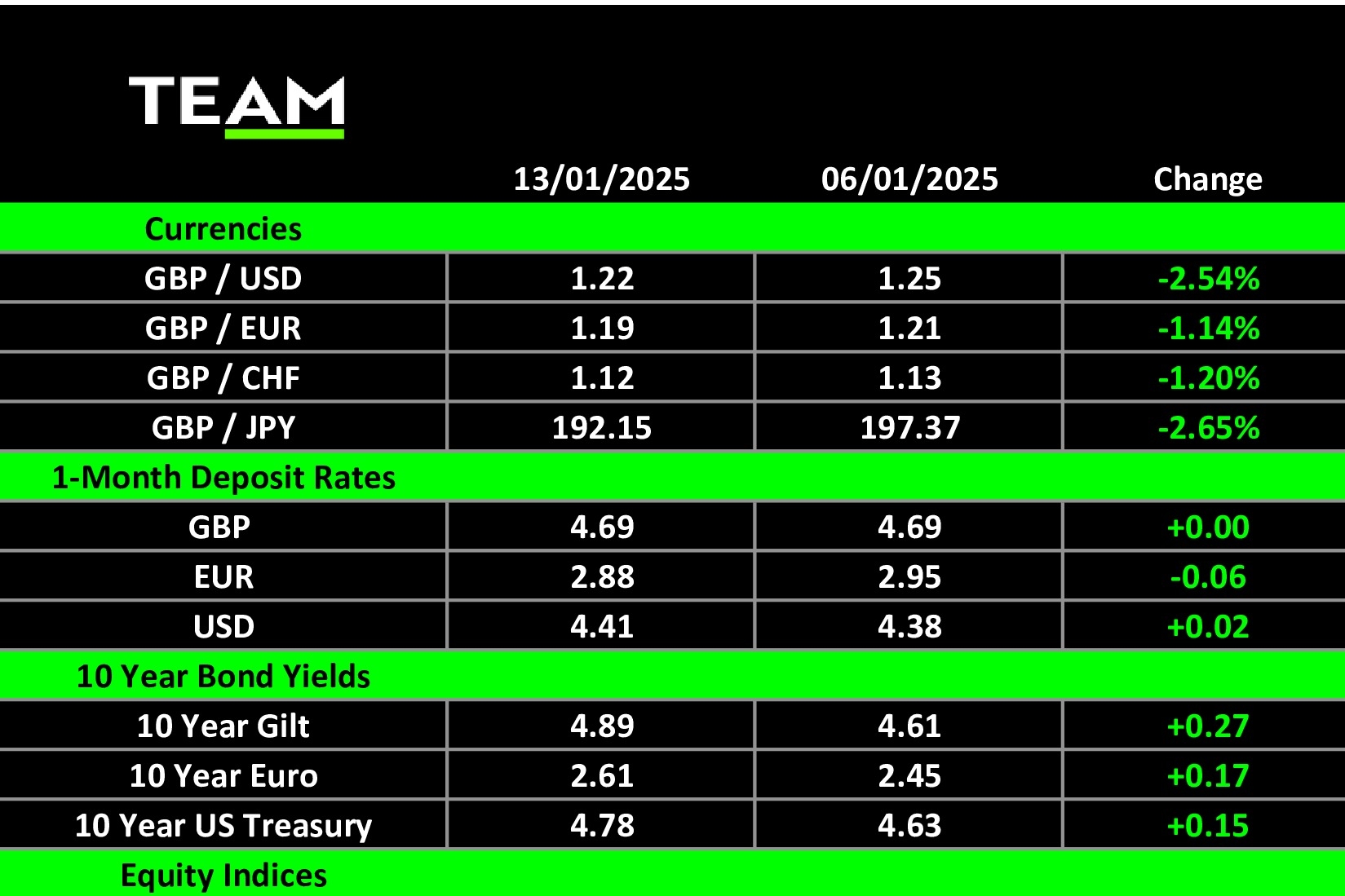

Several pieces of American data released during the week also fuelled concerns about a return of inflation. The doozy was Friday’s payrolls data which showed that the US economy had added 256,000 jobs during December, well ahead of consensus expectations (+155,000), while the unemployment rate dropped to 4.1% versus survey expectations of 4.2%.

Treasury yields ripped higher (bond prices move inversely to yields, dropping sharply), as money markets adjust their expectations over the prospect of rate cuts in 2025 and where the longer-term rate of interest, or “neutral” rate, should be. It is worth noting that just one quarter-point rate cut is currently anticipated this year from the Federal Reserve versus four (or more) cuts just a few months ago.

Meanwhile, closer to home, Chancellor Reeves took the perplexing decision to visit China in pursuit of a strategic deal at a time when long-term gilt yields are spiralling higher.

The crux of the issue is that markets are calling her bluff on the recently announced “tax and spend” budget, remaining highly sceptical that faster economic growth can fund the huge, planned increases in borrowing, especially in the absence of meaningful, exciting policies to stimulate business activity and investment.

A toxic combination of higher long-term interest rates and a sharp fall in sterling (touching $1.21 this week) has evoked memories of 1976 when the UK received an IMF bailout, or, more recently, the disastrous Truss “mini budget” of 2022. The dramatic spike in yields is estimated to have added £9 billion to the UK’s annual borrowing costs of more than £100 billion, virtually wiping out the chancellor’s £9.9 billion spending buffer.

In an era of QE and ultra-low interest rates, the annual debt interest bill fell to just £25 billion in 2020-21 but even before the latest rise in yields, the UK Office for Budget Responsibility forecast that debt interest payments would average £112 billion a year between now and 2030. Ten-year gilt yields have risen to 4.9%, the highest since the 2008 financial crisis, and 30-year gilt yields to 5.5%, the highest since 1998.

The bond vigilantes are back. Your move, Chancellor.

Outside major asset markets, the devastating wildfires engulfing the City of Angels have propelled the natural disaster to contender for the most expensive in history.

Given the enormous clean-up operation, subsidies to those affected, and significant loss of tax revenues to Los Angeles for the foreseeable future, the municipal bond space has been thrust into the spotlight as market observers watch for a sign of contagion spillover.

Within commodities, the yellow metal continues to shine despite a big move higher in the dollar, underpinned by strong central bank demand for physical gold as a strategic asset, while oil was the big winner of the week, soaring on the heels of additional Russian sanctions and a cold winter vortex.