Sponsored Content

Harry Brassington, of Team Asset Management, offers a weekly round-up of global markets

The 2024 bull stampede continued this week as Beijing officials declared their own version of Mario Draghi’s infamous “whatever it takes” moment, unleashing a wide-ranging series of monetary- and fiscal-stimulus measures in a bid to shore up investor confidence.

The People’s Bank of China announced significant cuts to bank reserve requirements and a key lending rate, a slew of property-related measures designed to stimulate activity in the troubled sector, and liquidity support for China Inc.

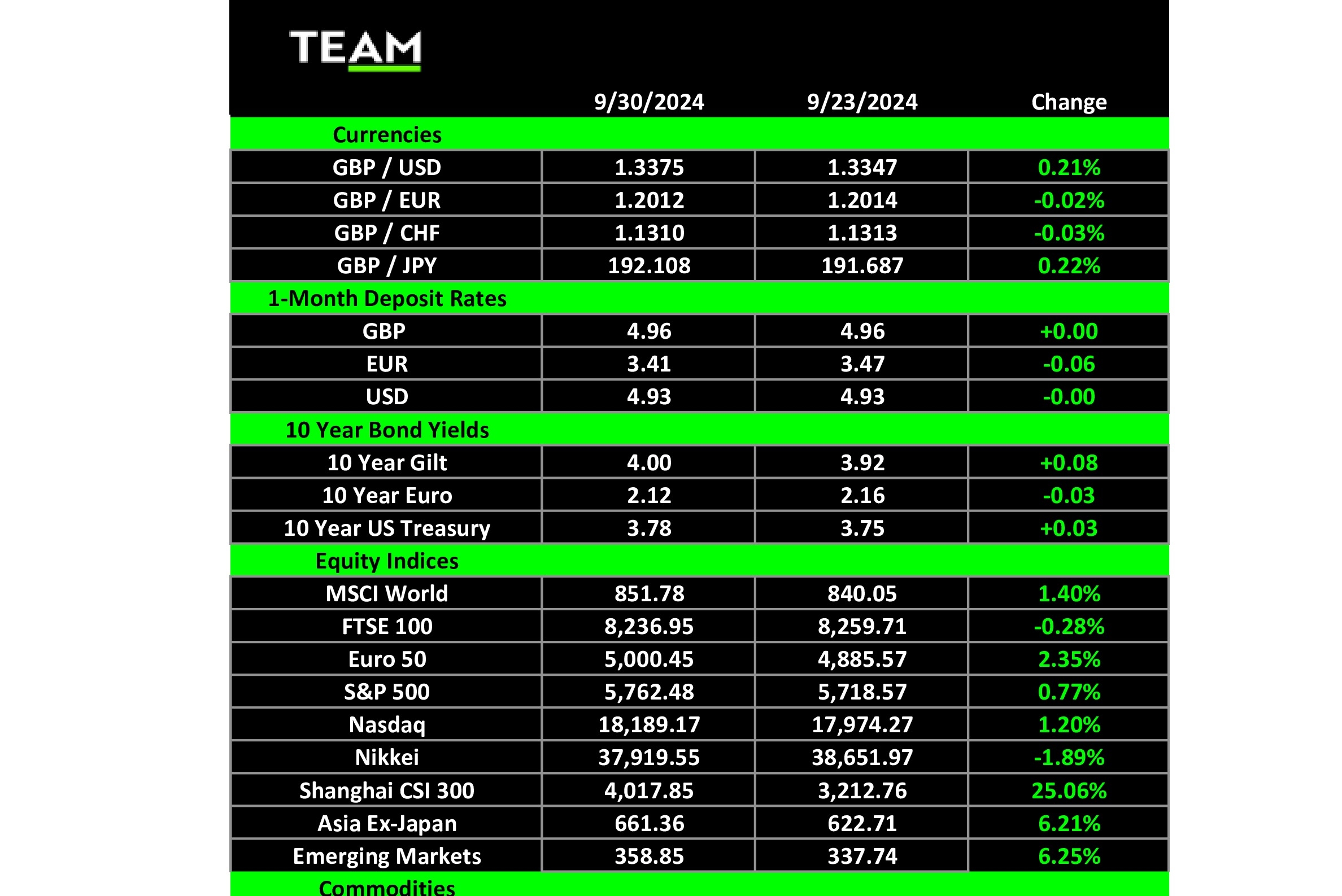

Mr Market’s ability to confound and surprise is one of the few constants in the investing world. Having registered 52-week price lows less than a fortnight ago amid a widespread sense that China has become “un-investable”, the domestic Shanghai and Shenzhen indexes soared to touch new 52-week price highs on Monday, enjoying their best week since 2008.

Chinese e-commerce giants Alibaba, JD.com, and PDD all surged, while property and consumer stocks also rallied ferociously.

China’s news acted like a steroid injection for risk assets, with sectors and companies that have been hurt by the country’s economic slowdown this year now benefitting from the pivot towards improving domestic consumption and industrial activity.

Mining stocks, including Antofagasta, Anglo-American, Glencore and Rio Tinto, led the gains in Europe, benefitting from what is likely to be significantly increased demand for commodities.

In the US, markets also received a boost from a benign reading from the Federal Reserve’s preferred inflation measure, the personal consumption expenditure (PCE) index, which rose just 0.1% month-on-month in August. This implies the Fed can push on with further interest rate cuts and engineer a soft-landing for the US economy.

Closer to home, the UK’s economic challenges have dominated recent headlines, with the recently installed Labour government grappling with high debt, sluggish growth, and limited options for public investment. The national debt now exceeds 100% of GDP, and borrowing reached £64.1 billion by August. The Labour Party kicked off its annual conference amid a political row involving donations, back tracking on the non-domicile rules, and PM Keir Starmer’s “bring back the sausages” moment.

In corporate news, Micron Technology surged over 18% following its earnings announcement, benefitting from strong annual results driven by rising demand for artificial-intelligence applications in data centres, despite declining PC and smartphone sales. With doubts lingering over whether the super-charged growth the AI sector has witnessed over the past two years can be sustained, Micron’s results were well received by investors.

Intel also rose nearly 10% on rumours of a potential acquisition by Qualcomm, providing some relief during a challenging period for the company, which has lost over half its value this year.

Luxury brands like Burberry rallied nearly 17% following the announcement of China’s stimulus measures. LVMH was also in the news after it announced it had bought a 10% stake in Double R, the investment vehicle behind fellow luxury brand Moncler, well known for its down jackets which can cost more than £5,000.

In the commodities sector, gold continues to shine, with the price touching new all-time highs in many major currencies. Indeed, this is gold’s best ten-month start to a year this century. News that Saudi Arabia has joined the list of central banks quietly accumulating significant holdings of the yellow metal underpinned sentiment, as did the tragic events unfolding in the Middle East, which are, naturally, creating a flight to haven assets.

In contrast, oil prices fell as Saudi Arabia shifted its strategy away from its $100-per-barrel target by restricting supply to balance its books. However, in a sharp U-turn, the world’s largest exporter will bring back production to normalised levels from December and seek to increase revenues by regaining market share.

Turning to the week ahead, the US jobs report has replaced inflation readings as arguably the most important data release for market watchers. If Friday’s nonfarm payrolls report reveals that fewer jobs were added in September than the 142,000 in August, it may fuel concerns that the US economy is slowing down, possibly towards recession.