Sponsored Content

David Gorman of Team Asset Management offers this week’s market review

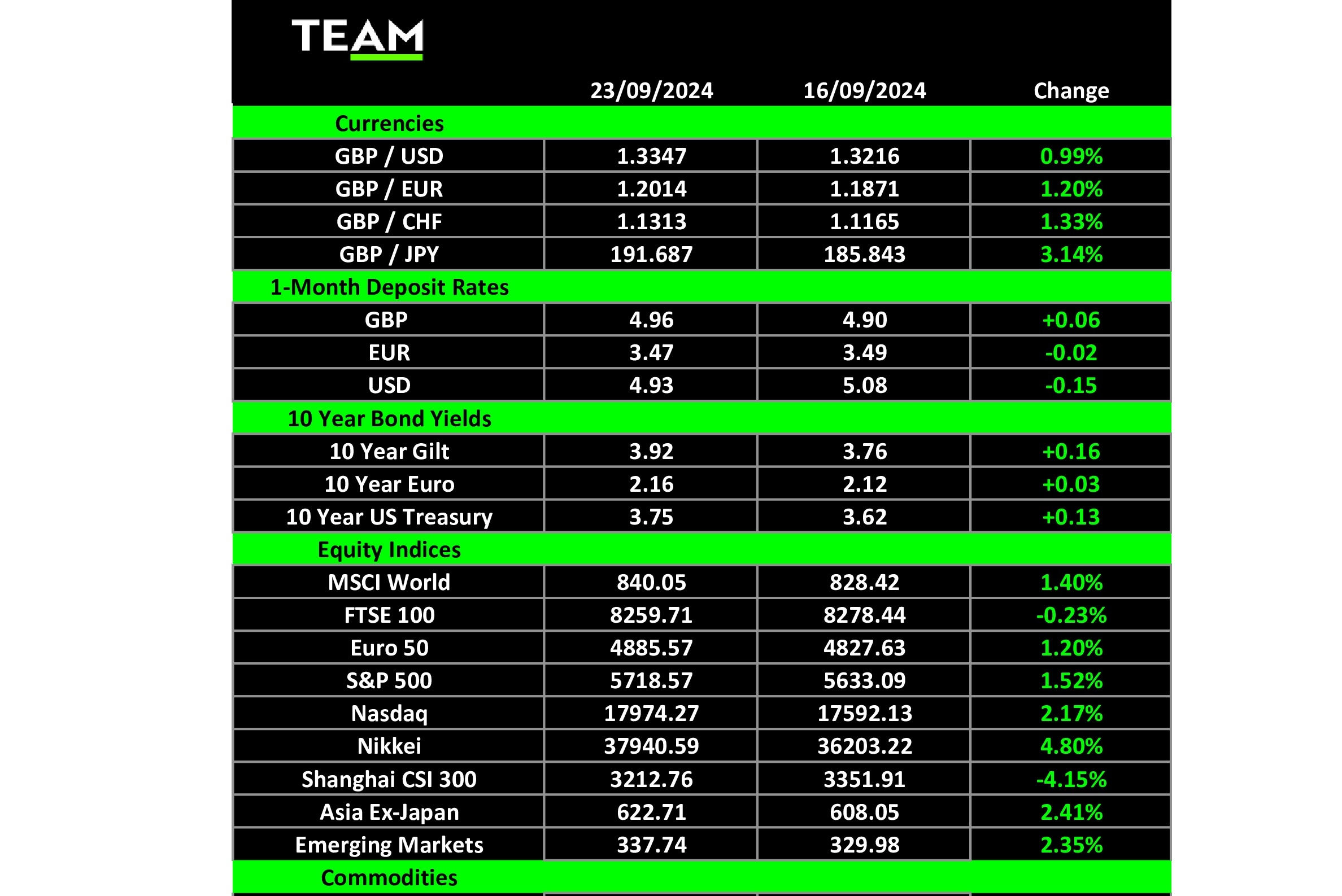

IT was a week of big rate decisions. The long-awaited US Federal Reserve move was to cut interest rates by 50 basis points (one half of 1%). However, the Bank of England kept rates unchanged, and both the Bank of Japan and People’s Bank of China decided to do the same.

The Federal Reserve Open Market Committee went big with 50 basis points, as policymakers said they saw more risks to employment levels while inflation goals were in better balance. The FOMC is pencilling in another half point of cuts this year, suggesting 25 basis point cuts at each of the next two meetings.

Donald Trump, the Republican nominee for President on the 5 November 2024 election, will think the move is politically motivated, helping Kamala Harris and the Democrats look better. Looking longer term, the committee feels that a gradual decline in rates from the current 4.75/5% level towards 2.75/3% is expected by 2026.

What concerns the market is how quickly the interest rate cutting cycle will unfold. Also, observers were surprised that all but one FOMC member approved the half-point cut when most evidence suggests the US economy is not too hot but just right. Do they know something the market does not? The most worrying recent data point is a report summarising current economic conditions which showed only three of 12 districts achieving growth in the past two months.

History tells us that when a rate-cutting cycle begins, equity markets move strongly forward over the next year or two. This has applied 85% of the time in the last 20 cycles. During the 2000 and 2007 rate-cutting cycles, there were noticeable negative equity returns over the next two years. At present, despite the broad US equity market reaching record highs, investors remain uncertain and confused over whether the larger rate cut is an omen for trouble or a recession ahead.

It will become clearer over the next few weeks but, typically, sectors such as consumer discretionary, construction, utilities and energy should see relative progress to the main market. If not, investors may be telling us something about where they think the economy is going.

With dollar interest rates now becoming less attractive, there has been a move out of the US currency with sterling moving from $1.23 in April this year to $1.33 today – an 8% positive move.

A prime beneficiary has been the price of gold, which has reached an all-time high and is now up 26% since the start of the year. It is fascinating to think that the UK government sold 50% of its gold reserves (12.7m ounces) between July 1999 and March 2002 at an average price of $275 per ounce. During that time, gold was priced at its lowest level for 20 years but Gordon Brown, the Chancellor of the Exchequer, still pursued the exit following the route of other central banks. This has cost the UK over $26bn (today’s price is $2,628) in lost assets but that unfairly assumes the replacement foreign currency assets have not added any value. Traders have dubbed this time “Brown’s Bottom”. Let us hope that the new Chancellor, Rachel Reeves, is not so infamously remembered for her decisions.

Turning to corporate events, FedEx shares, a good barometer for economic activity, stumbled 15% on Friday, their biggest one-day fall in two years, as its latest quarterly results were much weaker than expected and may justify the big cut by the Fed. The Memphis-based delivery giant revealed that many customers continued to trade down from speedy to cheaper, slower delivery options and it has work to do in reducing costs after investing heavily during the pandemic the meet surging demand.

Elsewhere, according to Bloomberg sources, Johnson & Johnson raised its settlement offer to over $8.2bn for the myriad lawsuits claiming its baby powder led to cancer, and Nike shares rose nearly 10% as investors welcomed the arrival of a new chief executive, Elliott Hill, although he is not so new as he is returning to the company after an earlier 32-year period. Confidence is high that he can reinvigorate the workforce and a brand that has lost market share to its rivals.

Key events this week are thin on the ground, but the Federal Reserve’s preferred inflation measure is released on Friday, as is the Michigan Consumer Confidence index.