Sponsored Content

Matthew Boxall, of Team Asset Management, offers this week’s market review

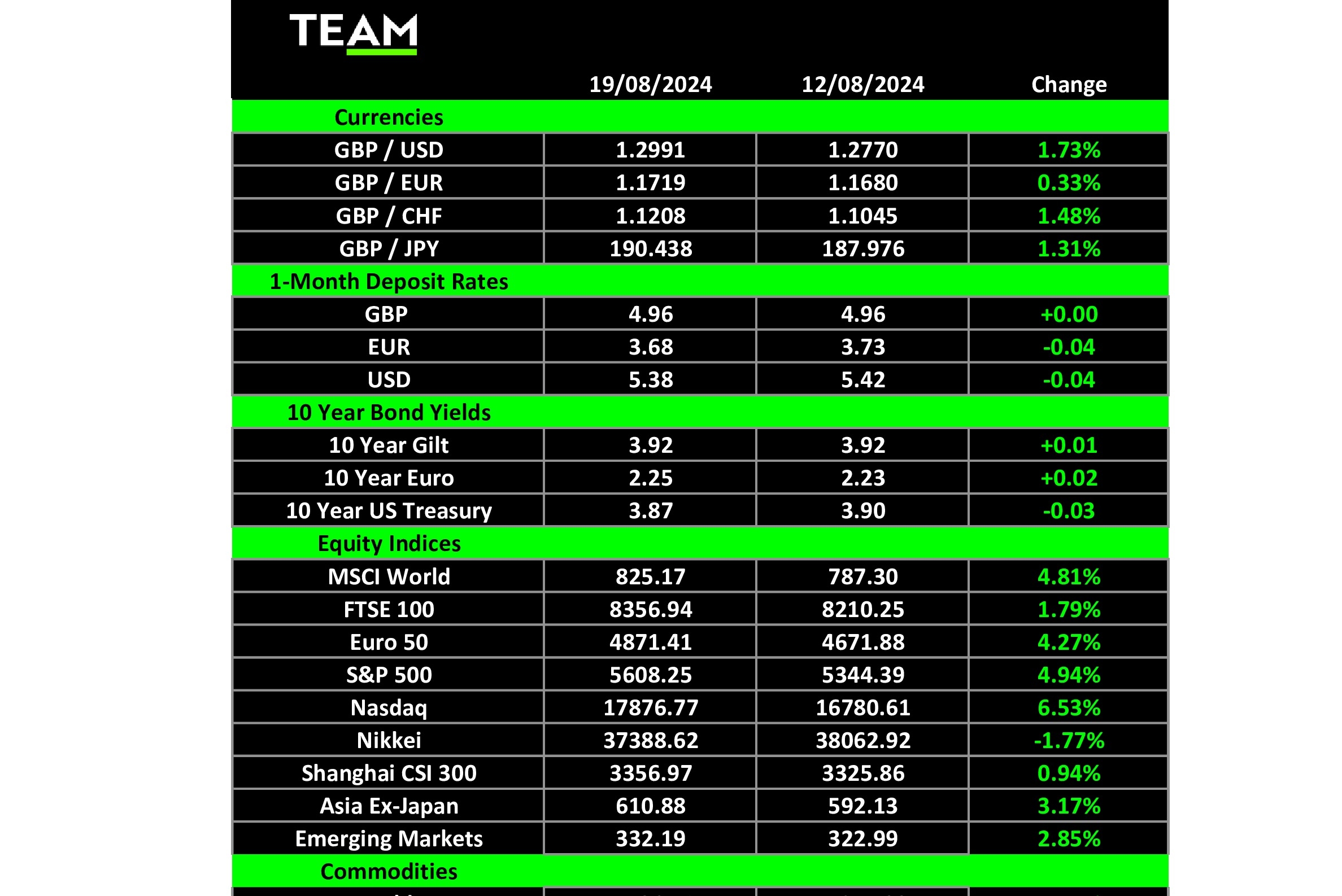

WHAT a difference a week makes. The S&P 500 bolted to its best weekly advance since October with a 4% gain, breaking a four-week losing streak.

The tech-heavy Nasdaq closed 6.5% up, the UK’s FTSE 100 1.8% up and Europe’s STOXX 50 4.3% up on the week.

Economic data from around the globe brought peace, particularly the better-than-expected US inflation reports for July. Headline producer prices rose 2.2% year-on-year, down from 2.7% recorded in June, and annual consumer price inflation slowed to 2.9% year-on-year. The downward trajectory of inflation reinforced expectations that the Federal Reserve would be able to start cutting interest rates next month.

In the UK, annual consumer price inflation increased for the first time since December, rising to 2.2% in July from 2.0% in June. The headline rate was expected to increase as energy bills fell by less last month than in July 2023, but it was lower than consensus forecast of 2.3%. The increase is unlikely to concern policymakers at the Bank of England who voted to cut interest rates from a 16-year high of 5.25% earlier in the month and are expected to reduce rates further before the year-end.

A strong US retail sales report for July, and bumper quarterly earnings from Walmart also helped to ease fears that the world’s largest economy is on the brink of recession. The retail giant generated revenue of $169.3 billion in the second quarter, a 4.8% increase from the same period last year, and chief executive Doug McMillon asserted that “we aren’t experiencing a weaker consumer overall”.

Elsewhere, confectionery giant Mars announced that it had agreed a deal to acquire Kellanova for $35.9 billion, or $83.50 a share. Kellanova, whose products include Pringles, Pop-Tarts and Cheez-It, was created in 2023 after Kellogg separated its breakfast cereals and snacks businesses.

Starbucks has endured a difficult 2024, reflected by a 20% fall in its share price on the back of disappointing earnings. The downturn attracted the attention of activist investors, including Elliott Global Management, who have built up stakes in the coffee chain and their pressure came to bear last week as Starbucks dismissed chief executive Laxman Narasimhan, replacing him with Chipotle’s Brian Niccol.

The market response was immediate, with Starbucks rallying 25% on the day of the announcement while Chipotle shares fell 8%. Why? Because since Niccol took over Chipotle in 2018, the stock has risen 770% and investors are hoping he will bring the same recipe of success to Starbucks.

In commodities markets, warnings of a “harsh winter” in China’s steel sector pushed the price of iron ore down to a two-year low, wiping $100 billion off the market value of the big four iron ore miners – BHP, Rio Tinto, Vale and Fortescue. The prolonged downturn in the country’s property sector has suppressed demand for steel, and mills are under pressure to cut production to reduce the current glut of the construction metal.

Gold, propelled by US rate-cut hopes and geopolitical concerns, climbed above $2,500 per ounce for the first time ever. The war in Ukraine, the conflict in the Middle East and the increased tensions between the US and China all point towards continued demand for safe-haven assets in the short to medium term.

In the crypto markets, Bitcoin returned 0.4% over the week. Politics played another role in the digital asset space, where crypto Democrats have formed the group called Crypto4Harris, to rally behind Kamala Harris in the upcoming election. Billionaire Mark Cuban, financier Anthony Scaramucci, congressman Adam Schiff and other crypto advocates also hope that Harris will take a more pragmatic stance on the sector than President Biden. Both parties are trying hard to win over the crypto enthusiasts ahead of the upcoming election.

Looking ahead, investors’ eyes will be on the Federal Reserve’s Jackson Hole symposium tomorrow and Friday where economists, politicians and central bankers come together to discuss long-term policy issues. The most anticipated speech will be that of Fed chair Jerome Powell for comments on the likely path of US interest rates.