Sponsored Content

Lloyd Adams, of Team Asset Management, offers this week’s market review

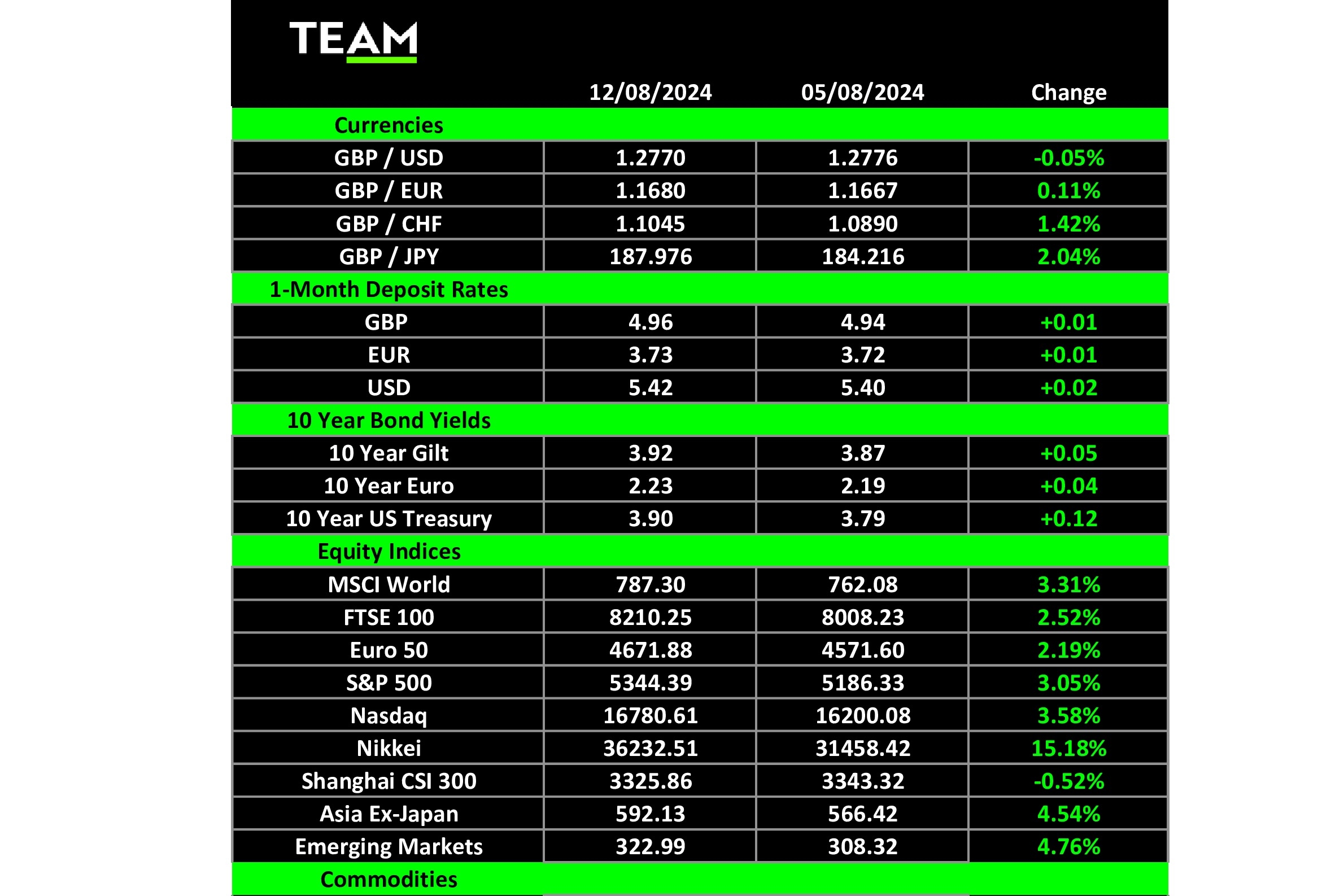

THE Japanese Stock Exchange (Nikkei) experienced significant volatility early last week, following Japan’s first interest-rate hike since 2016.

This move strengthened the yen, negatively impacting Japanese exporters and signalled an end to the “carry trade”, borrowing in a currency with a low interest rate, such as yen or Swiss franc, to invest in higher-yielding assets elsewhere.

Japan plays a crucial role in global liquidity, with Japanese investors holding about $3.5 trillion in international assets as Japanese banks’ foreign lending has increased by 20% over the past two years to around $1 trillion.

After this initial shock, global markets stabilised, buoyed by positive US employment data which suggested fears of a recession are overblown. The CBOE Volatility Index, which signals the level of fear or stress in the stock market, also eased from its pandemic-era highs.

This calming effect reduces the immediate pressure on the Federal Reserve to act, although money markets are advocating a rate cut at the central bank’s next meeting in mid-September, and possibly another two cuts before the end of the year.

Shipping container companies are often seen as a barometer for demand in global trade and AP Moller-Maersk provided more reassurance that a recession isn’t imminent, indicating that US freight demand remains strong. It noted that US inventories are elevated but not concerning, and retailer orders continued to show robust demand.

The Paris Olympics have significantly boosted France’s economy, with an estimated $12 billion (11.1 billion euro) in long-term impact. The Games set a record for ticket sales and a surge of 1.73 million tourists in the first week.

Parisian hotels experienced a 206% increase in weekly revenue per room and a rise in occupancy to 85.4%. Organisers hope that the Games will provide lasting economic benefits for France and Europe.

In commodities markets, oil posted its first weekly gain since early July amid ongoing attention to how Iran will react to the recent assassination of Hamas and Hezbollah leaders. The longer-term picture, however, is different and OPEC lowered its global oil demand growth by 135,000 barrels a day to 2.1 million a day in 2024.

Gold also attracted inflows, nearing its all-time high set last month. The precious metal has been buoyed by strong central bank purchases and robust demand from Chinese consumers.

Moving to company highlights from the last week, BT shares rose 7% on Monday following the announcement that Bharti Global has agreed to acquire a 24.5% stake from Altice. Shares in Shopify have risen 27% since the e-commerce platform reported a surge in second-quarter revenue and provided a strong third-quarter outlook for profit expectations. Axon (+24%), known for its Taser devices and police body cameras, was another winner after reporting better than expected earnings.

Some losers for the week included Super Micro Computer (-18%) on concerns over the high costs for AI server chips. Monster Beverage (-10%) fell after second-quarter results missed expectations and shares in Airbnb (-10%) declined following a disappointing forecast for the next quarter, reflecting a slowdown in US tourist demand.

Looking to the week ahead, today’s US inflation report for July will be a key focus for investors as it will shed more light on when the Federal Reserve will start cutting interest rates. Most analysts expect annual CPI inflation to hold steady at 3% but a deviation higher or lower could trigger more volatility across financial markets.

The Office for National Statistics will also release the UK’s inflation report for July on the same day. Annual consumer price inflation is expected to rise to 2.3% in July, up from 2% in May and June, as the impact of lower energy bills diminishes. A higher level will complicate the Bank of England’s plans for further interest rate cuts.