Sponsored content

Craig Farley, of Team Asset Management, offers this week’s market review

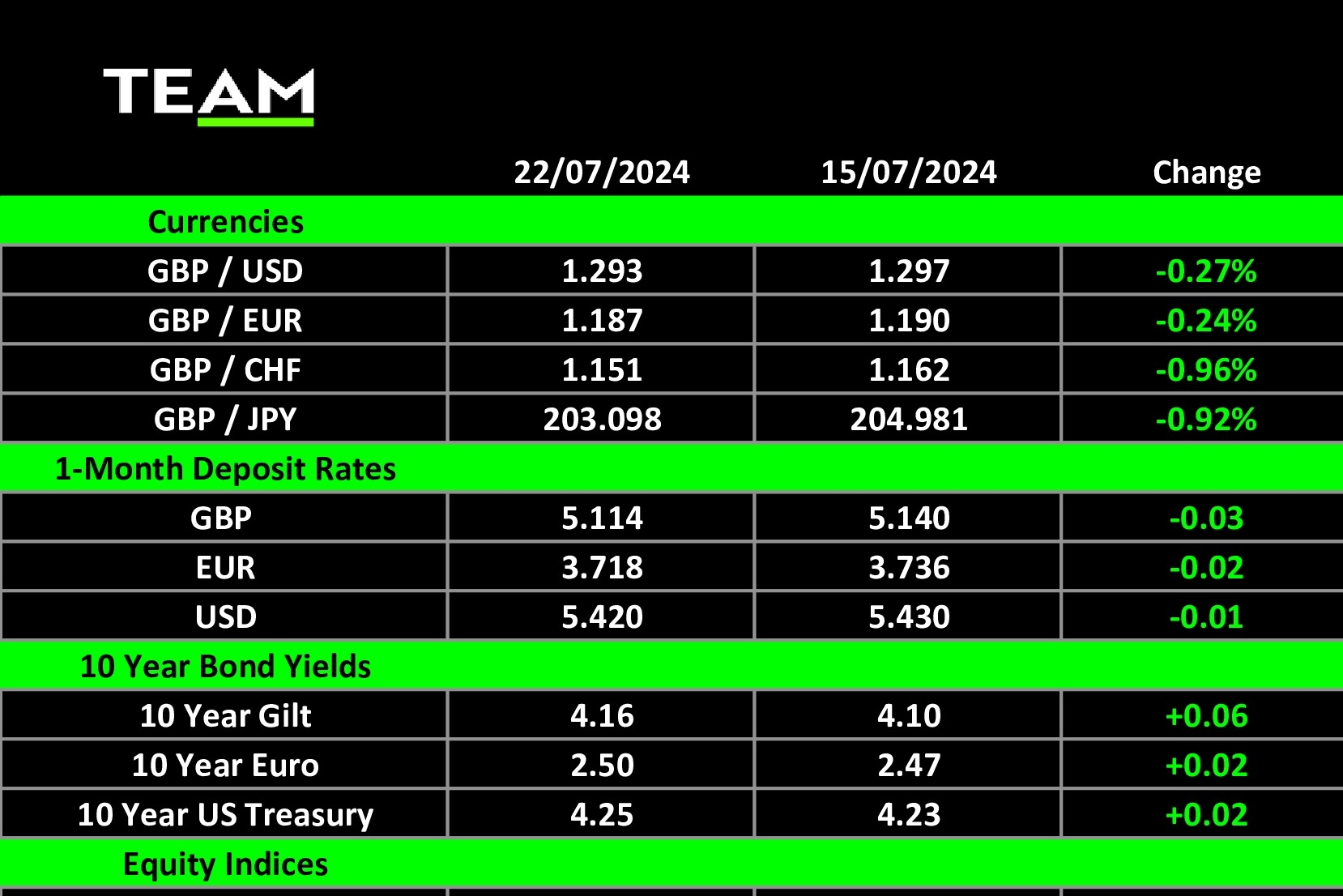

VOLATILITY re-emerged from the shadows this week, flaring up amid a sharp rotation away from the post-pandemic winners of this cycle (AI-related technology shares) and towards smaller-cap and value companies. Notably, this marked the third-best week of small cap outperformance over the bellwether large-cap S&P 500 index since 2000.

Identifying a protagonist for the rotation is usually a fool’s errand, for the true reason will only be known in hindsight. Nevertheless, the remarkable outperformance of mega-cap technology shares, deeply concentrated positioning in the technology sector by global fund managers and euphoric sentiment regarding the prospects of these companies all indicated that a pause for breath, or something more acute, was likely over the summer months.

When the news can’t get any better for companies, then, by definition, it can only get worse, and markets have moved quickly to reflect a potentially softer outlook for growth companies this year.

Meanwhile, political events in America have dominated mainstream news headlines. The increasing likelihood of a Trump “clean sweep”, meaning Republican control of the presidency, the House of Representatives and the Senate, along with news that Trump will retain Federal Reserve chairman Jay Powell for the foreseeable future (if elected), has markets excited about the prospect of tax cuts and rate cuts, which should be good news for smaller companies and more indebted cyclical and industrial sectors.

In a seemingly shrewd political move, Trump selected Senator JD Vance as his running mate, forming an alliance that could help secure votes across the crucial swing states of the US industrial Midwest. Technology titan Elon Musk called the decision “a great choice” and said on his social platform X that the combined line-up “resounds with victory”.

The trading week closed out with an announcement from incumbent President Joe Biden that he would, following mounting internal party pressure, step aside from the US election race. Kamala Harris has now won enough support to become the Democratic candidate to challenge Donald Trump in the race for the White House, with the winner due to be announced in early November.

Pouring fuel on the “rotation fire” was startling news of the biggest IT outage in history, as countless businesses and individuals all over the world grappled with the dreaded “blue screen of death”.

The IT failure affected airlines, banks, broadcasters and healthcare providers from the US and Europe to Australia, Japan and India. It is another example of how a minor technical change, in this case CrowdStrike’s minor security update to the Microsoft operating system, can wreak widespread havoc.

CrowdStrike, a company unknown to most outside the IT industry, is one of the largest providers of endpoint security software, which protects connections between computer networks and remote devices, from laptops, phones and servers to retail payment terminals and cash machines.

In what may be regarded as a perfect storm for the technology sector, semiconductor chip makers, the darlings of this bull market, were aggressively sold off following news that the Biden administration had told allies it was considering severe export curbs if companies such as Tokyo Electron and ASML Holding continued to provide China with access to advanced semiconductor technologies.

In other corporate news, the world’s biggest watchmaker, Swatch Group, reported a sharp fall in first-half sales and earnings, as weaker demand in China heavily impacted sales, while European luxury goods company Hugo Boss plunged after cutting its sales outlook, also flagging challenges in China.

Looking to the week ahead, investors will be watching tomorrow’s scheduled release of the US government’s initial estimate of second-quarter GDP. The report is expected to show that the economy accelerated relative to the first quarter, with the whisper number of +2.7% doing the rounds. Corporate earnings season is also in full swing, and results and guidance from corporate America, including Alphabet and Tesla, will probably play a big part in determining the short-term path ahead for asset prices.