Sponsored Content

Lloyd Adams, of Team Asset Management, offers a weekly round-up of global markets

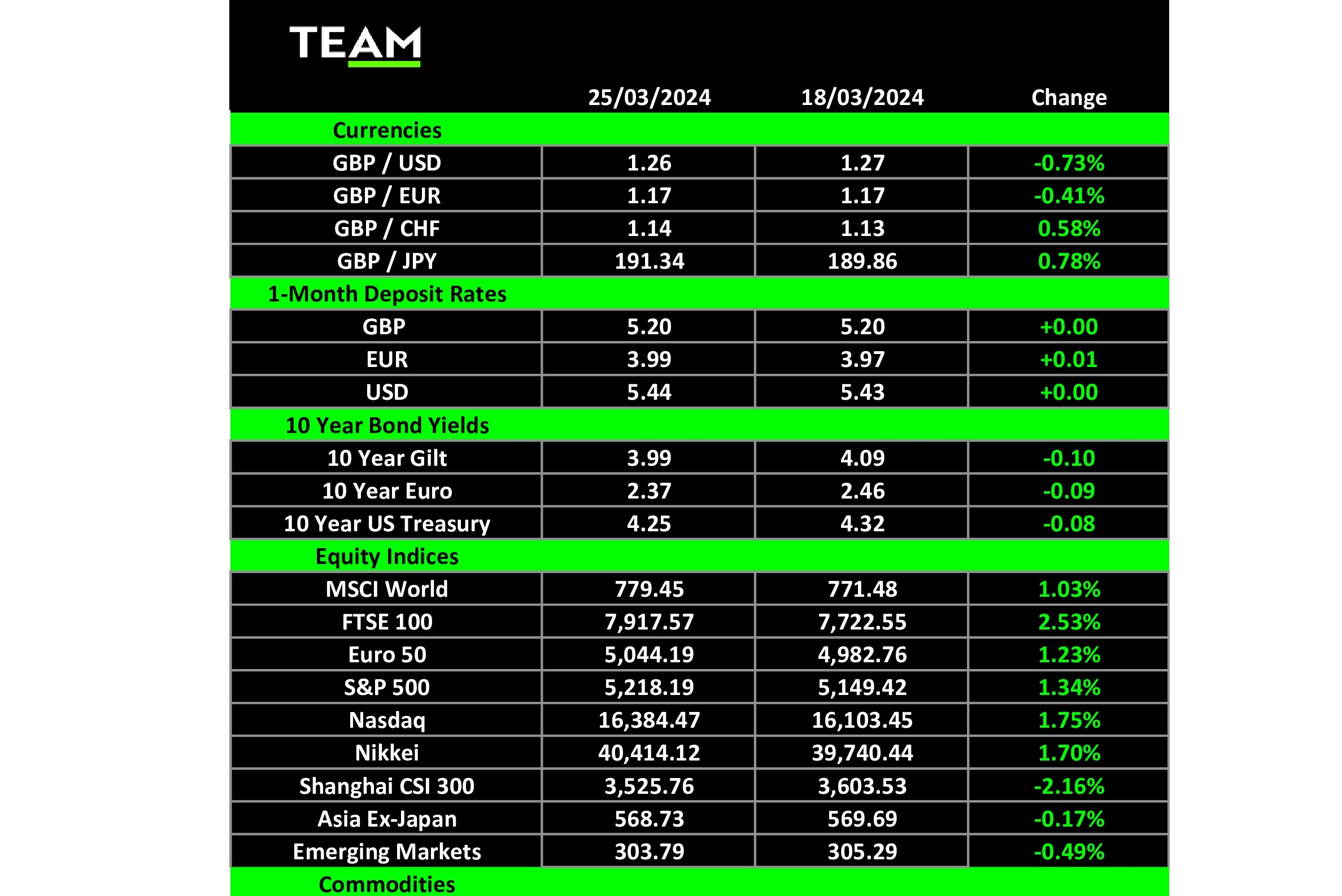

THE twists and turns started last week as the surprisingly dovish central banks triggered a surge in stocks and bonds on both sides of the Atlantic.

The Federal Reserve set the tone on Wednesday evening, signalling that it would cut interest rates three times this year despite also raising its economic growth forecast for 2024 to 2.1%.

On the back of some recent hotter-than-expected inflation and jobs reports, markets were a little nervous that the Fed would delay cutting rates, but chair Jay Powell stressed that there was probably some distortion from seasonal effects.

On Thursday, the Swiss National Bank surprised with a 25-basis point cut, taking its headline interest rate down to 1.50%. Switzerland avoided the inflation shock suffered by other developed economies and SNB chair Thomas Jordan revealed that policymakers expected inflation to remain below 2% for at least the next few years. The surprise move sent the Swiss franc tumbling to its lowest point versus the euro since July 2023.

Later in the day, the Bank of England announced it would hold interest rates at a 16-year high of 5.25%, but also suggested that rate cuts were not too far away. The two members of the Monetary Policy Committee who had been voting for rate hikes at previous meetings fell into line with the majority, while one member, Swati Dhingra, again voted for a cut.

BoE governor Andrew Bailey said that he was encouraged by recent inflation data and that, should it continue to move back towards the bank’s 2% target rate, there would be scope to start easing monetary policy. Markets now expect the BoE to match the Fed with three cuts this year.

The dovish turn sent sterling and UK government bond yields lower, while the FTSE 100 (+1.9%) had its strongest one-day performance since September 2023. A weaker pound is a positive for the FTSE 100, with companies in the index generating around three-quarters of their aggregate earnings overseas.

Although the FTSE 100 attracted inflows last week, Amsterdam solidified its grip on the title of Europe’s equity trading champion, holding on to the crown it took from London in July 2021 following Brexit.

In February, the average daily value of shares traded in Amsterdam reached 10.5 billion euros, compared to 8.95 billion euros in London, according to data from CBOE Global Markets. Paris and Frankfurt trailed behind in third and fourth place, with daily trading volumes of 5.6 billion euros and 5.0 billion euros respectively.

While most central banks have set the stage for lower interest rates, the Bank of Japan moved in the opposite direction last week, raising borrowing costs for the first time since 2007 and ended a period of eight years of negative interests.

The historic decision comes on the heels of significant wage increases at major Japanese firms, the strongest since 1991, and the decision was well received by investors, pushing Japanese stocks to new record highs.

The net impact of last week’s central bank moves was a stronger US dollar, weighing on commodities which are priced in dollars. Brent crude was also weaker on reports of a possibility of a Gaza ceasefire, which could ease geopolitical concerns in the Middle East.

However, offsetting these factors were concerns about potential disruptions to global oil supply due to Ukrainian attacks on Russian refineries. These strikes have reportedly taken out 7% of Russia’s refining capacity, or 370,500 barrels per day. Analysts warn that prolonged disruptions could force Russia to cut exports if storage limitations arise.

Gold prices also took a small tumble on Friday. The main reason for the dip? Once again, it was the strengthening US dollar, which makes gold pricier for those paying with other currencies.

Analysts believe this might be a short-term correction after a hot streak, with potential support around $2,148 per ounce. Silver, platinum and palladium weren’t so lucky. They all saw steeper declines on Friday and are looking at weekly losses too.