Sponsored Content

Craig Farley, of Team Asset Management, offers this week’s global market review

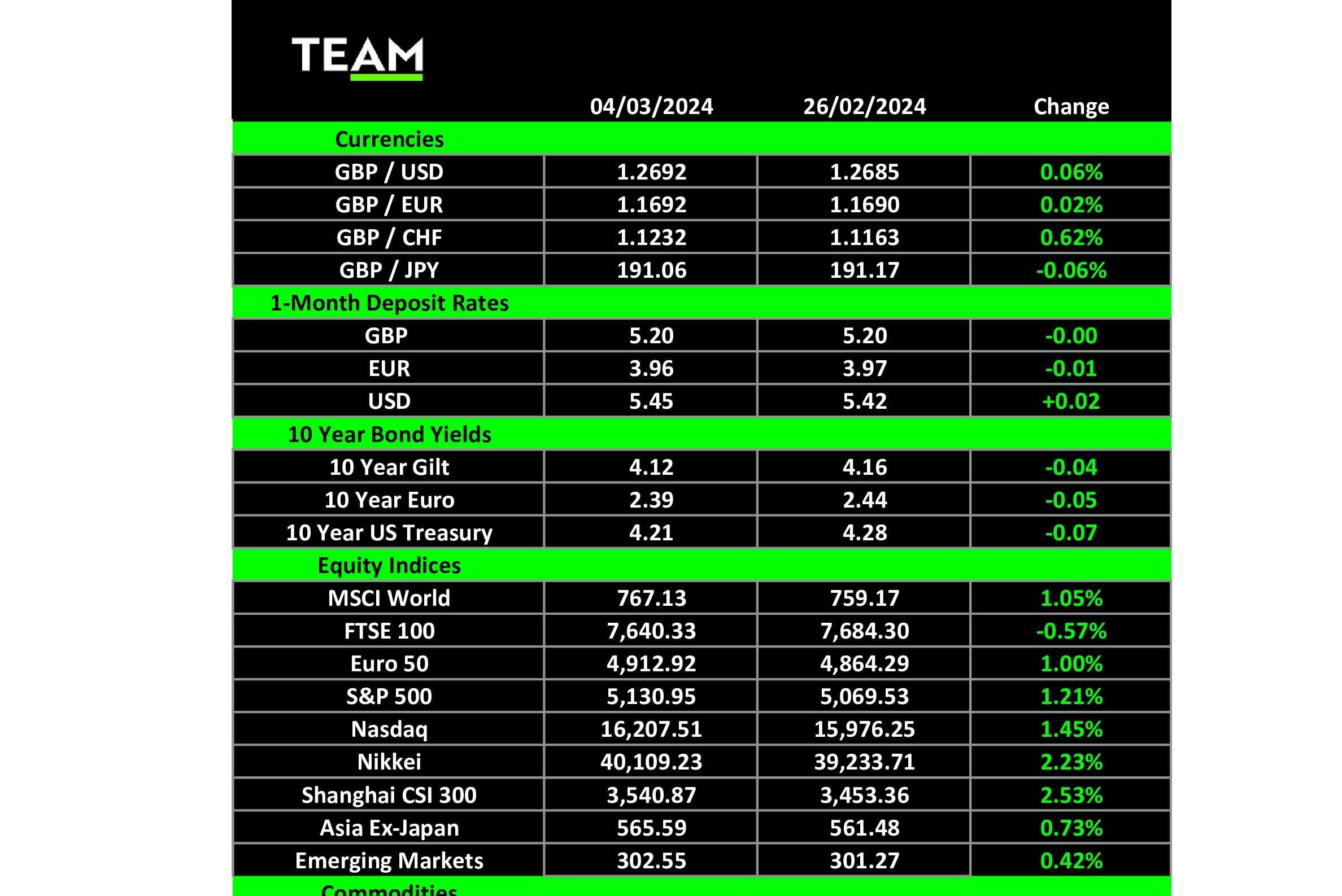

THE bull stampede continued in earnest this week as global equity markets surged higher, led by the US.

The S&P logged another 1.2% gain, while the technology-laden Nasdaq added 1.5%, to record new all-time highs. As it stands, 26% of S&P 500 index companies have registered new all-time highs so far this year, as elevated earnings expectations have been matched, particularly by the technology and e-commerce sectors. For those with access to a working DeLorean with flux capacitor, $5,000 invested in chipmaker Nvidia in 2000 would now be worth a cool $4.7m.

Prevailing market conditions are currently being viewed so favourably by investors that renewed stresses in the US regional banking sector have gone largely unnoticed. The share price collapse of New York Community Bank followed a company statement citing “material weakness in internal controls”, including risk oversight and risk assessment. To recap, NYCB is the institution that acquired Silicon Valley Bank in the aftermath of the regional bank meltdown no more than 12 months ago. It seems lightning can strike twice.

Renewed optimism on the path for interest rate cuts in 2024 appears to have been driven by the release of the Personal Consumption Expenditures Index, the US Federal Reserve’s preferred gauge for tracking inflation. Headline PCE, including the more volatile food and energy categories, increased +0.3% monthly and +2.4% on a 12-month basis, the slowest pace since March 2021. That said, there was enough in the data reports during the week to warrant a raised eyebrow for those inclined to believe that the last mile of winning the battle on inflation is going to be the most difficult. Core PCE (including food and energy) increased +0.4% monthly and +2.8% on a 12-month basis, while so-called super core PCE (excludes energy and housing) has risen at a +4.1% annualised rate in the past three months.

In addition to inflation, US personal income witnessed an unexpected jump to +1% on the month, well above expectations for +0.3%. A widely followed measure of home prices, the Case-Shiller 20-city US price index, registered another all-time high, an astonishing statistic given the backdrop of multi-decade mortgage costs, and one which points to the country’s chronic housing supply shortage. All told, it suggests that multiple interest rate cuts this year are not a fait accompli.

Outside the US, Japan was the standout performer, with the Nikkei Index eclipsing the 40,000 level for the first time. Japan’s representation in global equity indexes has diminished substantially over the past three decades, but a combination of excitement over corporate governance reform and the enhancement of shareholder returns through a combination of increased dividends and shareholder buybacks are creating renewed interest in the market.

In the commodities sector, gold quietly recorded a new all-time high in price terms, while Brent crude advanced to $83 a barrel, touching a two-month price high. The price rise comes amid a leak from various OPEC sources that the OPEC+ cartel will continue to implement voluntary oil supply cuts through the second quarter of this year to support prices.

Finally, in the cryptocurrency space, Bitcoin rallied spectacularly on the week to close above $67,000 on the back of heavy institutional demand. BlackRock’s spot Bitcoin ETF vehicle has attracted over $10 billion in its first month. Based on notional value, Bitcoin has surpassed the Russian Rouble to become the 14th-largest currency globally, just behind the Swiss Franc.

The upcoming Bitcoin halving in April could be the core catalyst for more high-ticket flows into the Bitcoin ETF.

Looking to the week ahead, US Fed Chairman Powell testifies before Congress today and a closely watched monthly jobs report is released on Friday. Investors will be scrutinising Powell’s language closely for any hints of moves toward rate cuts and the jobs report for signs of a change in trend. The unemployment rate has remained below 4% for 26 months, a stretch last accomplished in the 1960s.