Sponsored Content

Team Asset Management offer their weekly round-up of the global markets

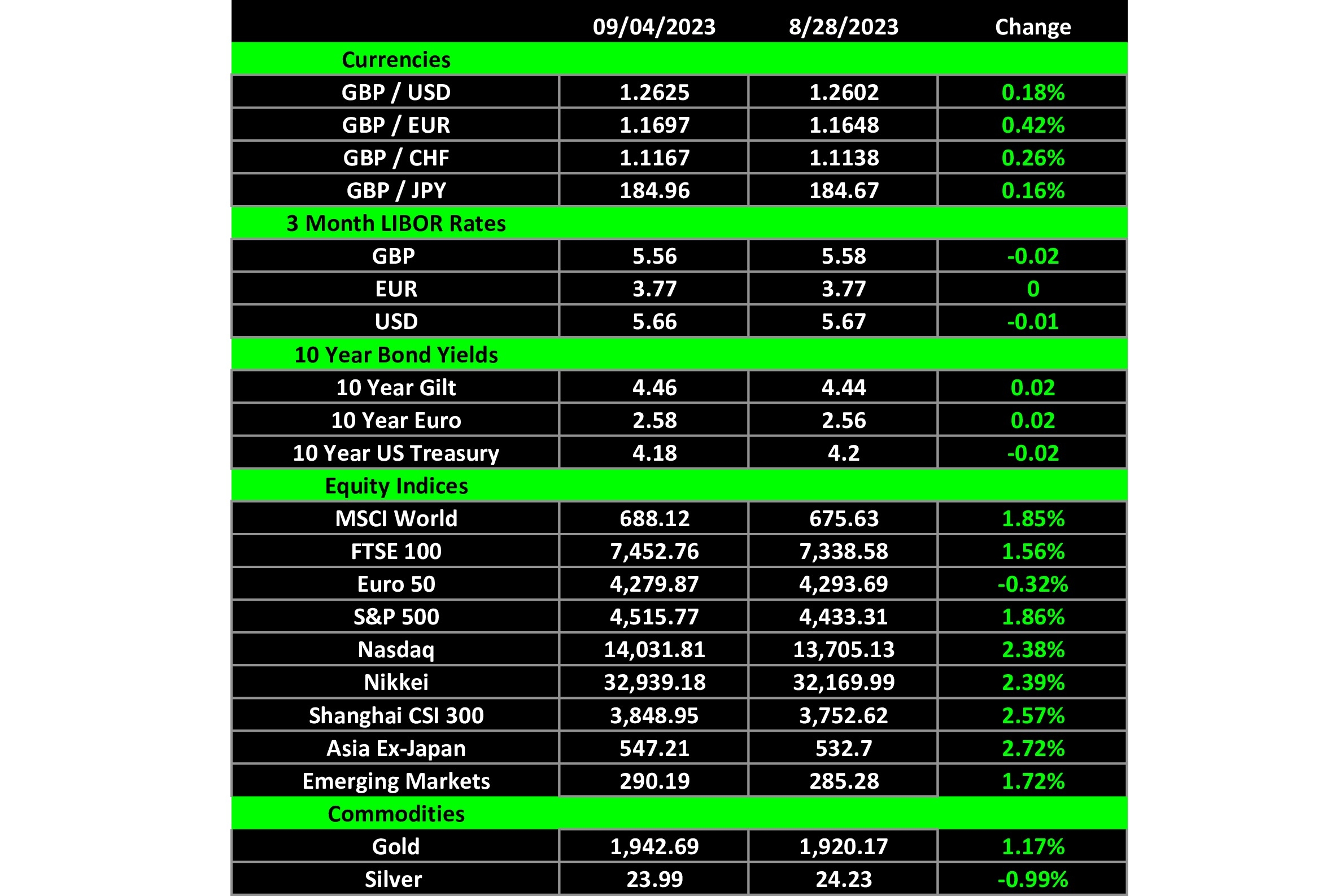

GLOBAL markets made a significant rebound last week after positive macroeconomic data helped revive investor confidence after what had been a painful August prior.

The S&P 500 finished the week gaining 2.5%. It was outperformed by its technology centric counterpart, the Nasdaq, which closed the week up 3.25%.

Declining government bond yields throughout the week had supported the march upwards for equities.

By Friday, the US ten-year Treasury yields, which acts a proxy for consumer inflation expectations, had sunk 4% before sharply reversing in the Friday-afternoon session, resulting in a small equity sell-off into the weekend as investors looked to take some risk off the table.

The recent trend of stronger-than-expected economic data, which had spooked markets this month, was alleviated in the US after reports of a softening labour market.

The number of job openings fell to 8.8 million in July, much below the consensus of 9.5 million and subsequently marking the lowest level since March 2021.

This is now the third month of decline and signifies a gradual slowdown in job supply after months of monetary policy tightening by the Fed.

This data was supported later in the week when the US unemployment rate shot up to recent highs of 3.8%, again above market expectations. This easing has bolstered sentiment among market participants as investors continue to look for a soft landing. With a softening labour market, the Fed may be more inclined to hold off from further rate hikes in anticipation of falling demand and lower inflation.

In other markets, Chinese equities had a noticeably dominant week on the back of stimulus hopes and a greater-than-expected retail sales figure, which was boosted by tourism. This helped piggyback other Asian and European indices with several consumer goods stocks, deriving sales from China, being helped upwards.

Brent crude climbed higher, surpassing $88 and reaching levels that have not been seen since November last year. Continued talk of the voluntary Saudi output cut spurred this move onwards, again posing the question of whether or not inflation will remain sticky as commodities begin to provide inflationary pressures.

Tesla shares fell 5% on Friday after more price cuts were announced, yet they still managed to gain 2.7% on the week. Tesla chief executive Elon Musk had previously said that the price of Tesla’s Full Self-Driving software would only ever go up in price, so it came as a surprise when the company dropped the cost by $3,000 from $15,000 in the US for customers who purchase up front.

Cryptocurrency also faced a volatile week despite finishing relatively flat. Prices jumped after a US court decided that the Securities and Exchange Commission should not have rejected asset manager Grayscale’s application to manage a spot Bitcoin ETF. Bitcoin proceeded to gain over 8%, with the rest of the crypto market following behind, but shortly gave back these gains by the week’s end when the SEC delayed its decisions on ETF approval.