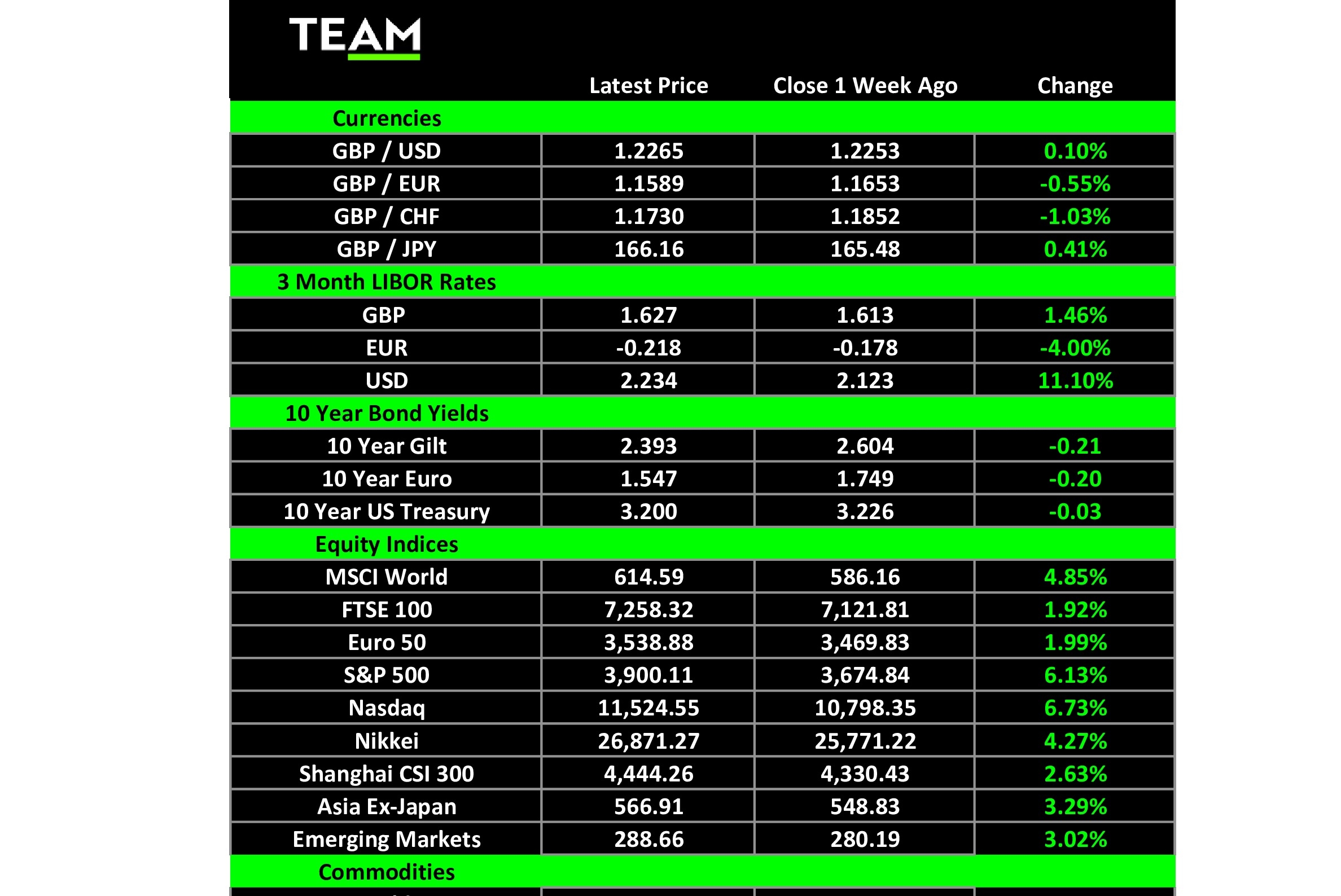

GLOBAL stocks ended a torrid run and climbed higher last week on expectations that weakening economic data would deter central banks from raising interest rates too aggressively. US markets led the gains with the blue-chip S&P 500 and technology-focused Nasdaq indices returning 6.1% and 6.7% respectively.

Chinese (+2.6%) and Hong Kong (+3.1%) stocks also had a good week, lifted by Shanghai’s city leader declaring victory against Covid. For the first time in two months of lockdowns and restrictions in China’s economic hub, no new infections were reported over the weekend.

Markets reacted to bad economic news positively, holding out hope that a deteriorating economic outlook would clip the wings of hawkish central banks and persuade them to slow the pace of interest rate hikes. Last week there was plenty of weak economic data to cheer.

UK consumers tightened their belts in May and the volume of retail sales fell 0.5% from a month earlier, driven by a drop in food shopping. The report published by the Office of National Statistics also revealed the value of overall spending increased 0.6% from April, a clear sign that consumers are buying less to offset higher prices.

Annual consumer price inflation in the UK reached a new 40-year high of 9.1% in May and Bank of England policy makers expect it to move into double digits by October. Catherine Mann, a voting member of the bank’s Monetary Policy Committee, warned that imported inflation from the pound’s near 10% fall versus the US Dollar this year was inflaming embedded domestic inflation.

Against this backdrop, it is not surprising that UK consumer confidence has fallen to the lowest since records began in 1974. The GfK confidence index fell to minus 41 in June, lower than during the financial crisis and the early stages of the pandemic. Any reading below minus 30 is associated with a recession.

Ford joined the list of large blue-chip companies to warn that ‘significant’ staff reductions were inevitable. After announcing it had chosen its plant in Valencia as its preferred site in Europe to build next-generation electric vehicles, the US car manufacturer revealed it would close another plant in Saarlouis, Germany. Ford also warned job cuts were to be expected in Spain as electric cars needed fewer staff to assemble them.

The weakening economic outlook has had a material impact on interest-rate expectations. Just a week ago, interest rate futures were pricing in the Bank of England’s base rate reaching at least 3.5% by May next year. Markets are now pricing in a rate closer to 3%.

A more benign interest-rate outlook is good for bonds, which had their best week since mid-March. The yield on ten-year UK government bonds fell 21 basis points to 2.39%.

It wasn’t such a good week for holders of Russian foreign debt. The 30-day grace period expired for Russia to make around $100 million of interest payments due on two of its foreign currency bonds, triggering its first default since 1998. Russia has plentiful foreign currency reserves, accumulated from its oil and gas revenues, but is frozen out of the global financial system.

Brent crude recovered some of its recent pull back and moved back above $115 a barrel despite the pledge from G7 leaders to work to curb energy costs at their summit in Bavaria. The US is leading an initiative to impose a price cap on Russian oil to restrict the Putin regime’s ability to finance its war in Ukraine.

Other commodities fared less well last week, including copper, which fell to its lowest level since the start of the pandemic. The industrial metal is often dubbed ‘Doctor Copper’ due to its ability to diagnose the overall health and well-being of the economy.