Sponsored Content

Lloyd Adams of Team Asset Management offers this week’s global market review

GLOBAL stock market performance was steadier this week, though ongoing geopolitical risks continue to cast a shadow. Investors are now shifting their focus to corporate earnings, with major reports expected from Amazon, Apple, and Microsoft, which have already pushed the Nasdaq technology index to new all-time highs.

The prospect of a global recession has now eased, with inflation steadily decreasing, according to the International Monetary Fund. However, while the economic outlook shows signs of improvement, global growth still faces challenges. Momentum remains steady yet lacks spark, driven by strong expansion in the US and parts of Asia. Long-term growth is expected to slow owing to challenges surrounding ageing populations and declining productivity.

Closer to home, a recent PwC survey suggests that a “vibecession” – a term describing downturns driven more by negative feelings than by actual economic facts or sense – could be looming in the UK. The survey reveals that many consumers are in a despondent mood about the general economic situation and plan to cut back on spending, particularly during Christmas. However, this sentiment stands in stark contrast with the IMF’s more optimistic outlook, expecting higher UK economic growth this year and next, aided by lower inflation. Economists also predict that the Bank of England will cut interest rates further.

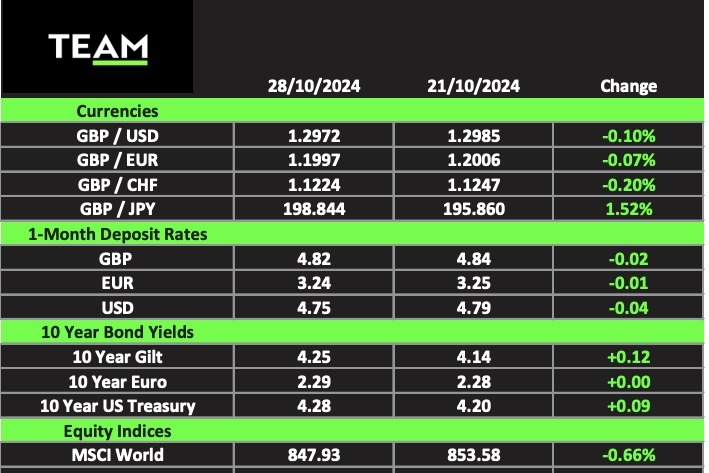

A surprise result in Sunday’s general election in Japan sent the yen tumbling to its lowest levels in three months. Recently appointed prime minister Shigeru Ishiba called a snap election to seal his mandate but instead his Liberal Democratic Party lost its parliamentary majority for the first time since 2009. Investors are now braced for months of political paralysis, with Ishiba vowing to stay on despite the defeat.

In company news, a strong quarterly earnings report and outlook saw Tesla shares jump 22% on Thursday, their biggest daily gain since 2013. Revenue generated by the world’s largest electric vehicle manufacturer rose 8% from the same period last year to $23.4 billion and chief executive Elon Musk predicted that vehicle sales could increase up to a third next year, owing to lower monthly financing payments for buyers and the “advent of autonomy”.

Musk asserted that Tesla’s Cybercab would definitely launch in Texas in 2025 and “probably” in California. He has also promised that the autonomous robotaxi will be available to buy for less than $30,000.

Shares in tobacco company Philip Morris gained more than 10% on Tuesday to a new record high after raising its profit forecast for 2024, supported by robust demand for anti-smoking products such as Zyn. The chewing-gum-like pouches have gained popularity among white-collar employees in the US and some users say that they have helped them to lose weight, dubbing it “gas station Ozempic”.

Losers included Michelin (-9%) after it lowered its annual targets owing to a decline in sales volumes across markets. The tyre manufacturer also warned that geopolitical tensions had disrupted logistics and supply chains. Shares in another French multinational, L’Oréal, fell 4% after sales growth in the third quarter missed analysts’ forecasts. It highlighted weaker demand for its skincare and make-up products in China in a challenging economic environment but hopes that expected government stimulus measures will improve consumer confidence.

In commodities markets, brent crude fell by $5 to $71 a barrel on Monday after Israel refrained from targeting oil facilities in its retaliatory strikes on Iran over the weekend. A measured initial response to the strikes from Iran’s supreme leader Ayatollah Ali Khamenei also appeared to reduce the likelihood of another round of tit-for-tat hostilities. With the risks of a disruption to supply easing, investors’ attention moved back to macro factors, such as a weaker outlook for Chinese demand and Saudi Arabia preparing to ramp up production of oil from 1 December.

Friday’s release of US nonfarm payrolls report for October will be a key focus this week, especially given its proximity to US elections and the Federal Reserve’s next interest-rate decision.