Sponsored Content

David Gorman of Team Asset Management offers a round-up of global markets

Only three weeks ago financial markets were complacent with record share index highs. In the last few trading sessions, dramatic, irrational, and highly chaotic moves have taken place. Just like children at Christmas with toys, investors who have been clamouring for interest rate cuts, and are now likely to get them in abundance, seem disinterested.

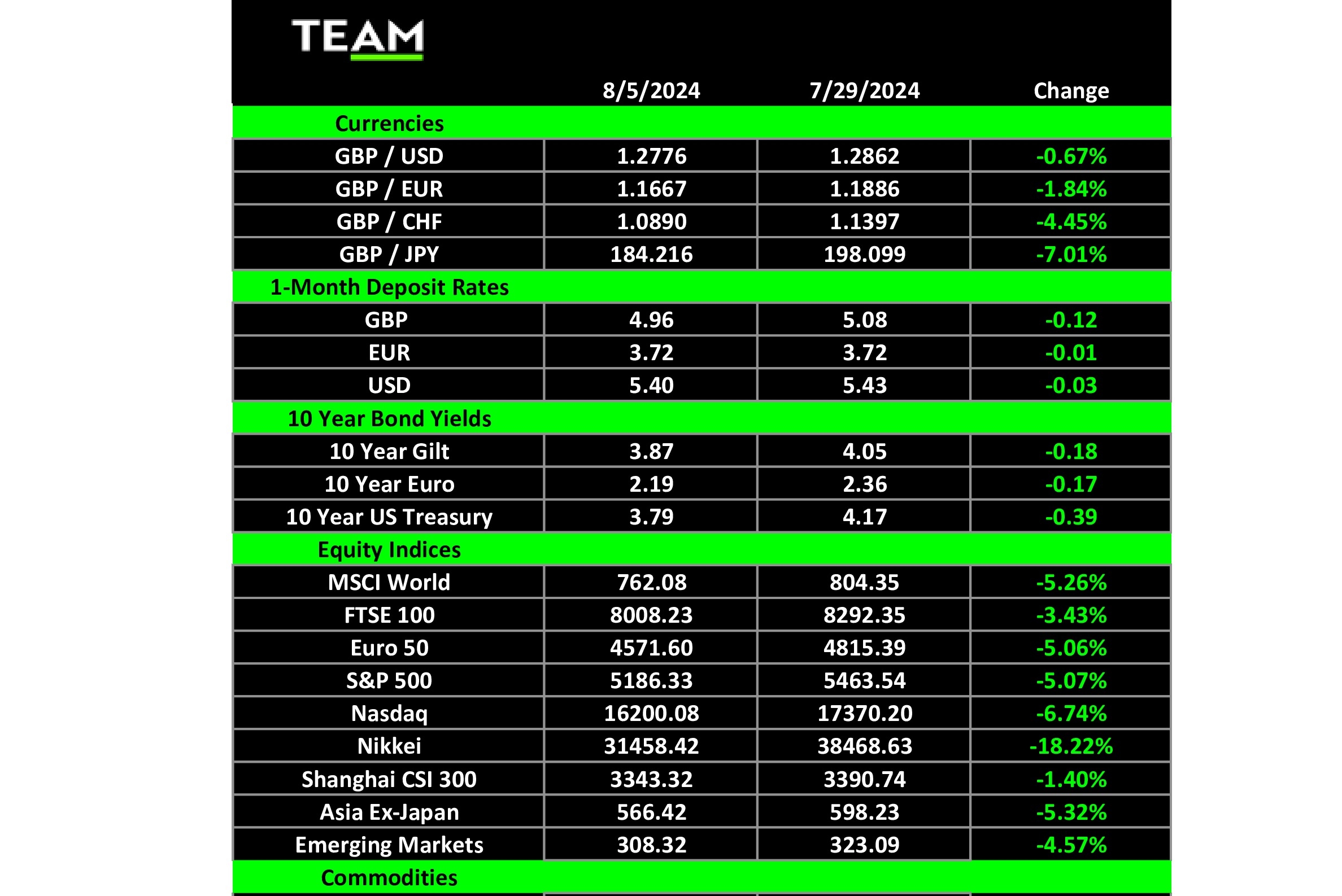

The Japan Nikkei 225 index on Monday had the largest point fall in history and in percentage terms the 12% fall was the largest since 1959. Japan fell 20% in the last two trading sessions. Momentum-driven markets such as technology and artificial intelligence areas were aggressively sold with the US NASDAQ and Russell 2000 indices more than 10% down and firmly in correction territory. The blue-chip S&P500 index is now 9% below its all-time high achieved on 16 July.

So, what has caused the disturbance? No one definitively knows. However, three key reasons appear uppermost.

Firstly, the Japanese central bank has kept its interest rate much lower than others through this cycle and allowed the Japanese Yen to consistently depreciate (until recently!). Investors took advantage of this to borrow Yen at almost zero rates and then invest the funds elsewhere – say in US technology stocks, Bitcoin or even US money markets where rates are still 5.5%.

This sounds great fun until the Japanese government decide to change policy and raise interest rates, driving the Yen back upwards and suddenly those investors who borrowed Yen must close their positions to avoid mounting losses. This action becomes a vicious circle for the markets to digest.

Secondly, market perceptions have changed from a resilient US economy, buoyed by artificial intelligence innovation, and falling interest rates, to a doomsday scenario of recession. This in turn was caused by weakening economic data, some poor high-profile corporate results, and surprisingly weak July employment data which for good measure had downward revisions for the earlier two months.

Finally, a geo-political event of the assassination of the Hamas leader in Iran has led to increasing concerns that Iran will retaliate against Israel, bringing closer the awful prospect of escalating Middle East conflicts.

One of the safe havens in all this carnage has been fixed interest investments where government paper has again acted as a safety net for investors. Last week the yield on a ten-year US Treasury was 4.15% but today it has fallen to 3.7% – a 10% increase in price and a 10% fall in yield. In early July, the money markets were discounting just one 0.25% US rate cut before the end of the year. Last night they were suggesting at least a cut of 1% including a 0.5% reduction at the Federal Reserve’s next meeting on 18 September.

At times like this genuine long-term investors need not panic but to stay calm and not overreact to volatility or the fear and risk aversion which has gripped markets. Sensible and professional guidance on asset allocation and strategy should be taken, as at times like these there are significant investment opportunities. Importantly, a shopping list of those investments you have always wanted to own, but haven’t due to high valuations, should now be considered.

Finally, we may see fireworks on 5 November 2024. The US Presidential election race seems like a 50-50 call between Kamala Harris and Donald Trump. The Democrats have been energised by the nomination of Harris and the standing down of Joe Biden. Important swing states are now “toss-ups” compared to just a couple of weeks ago when Donald Trump thought he could win easily against the incumbent. Things have certainly changed including another major investor uncertainty to consider.