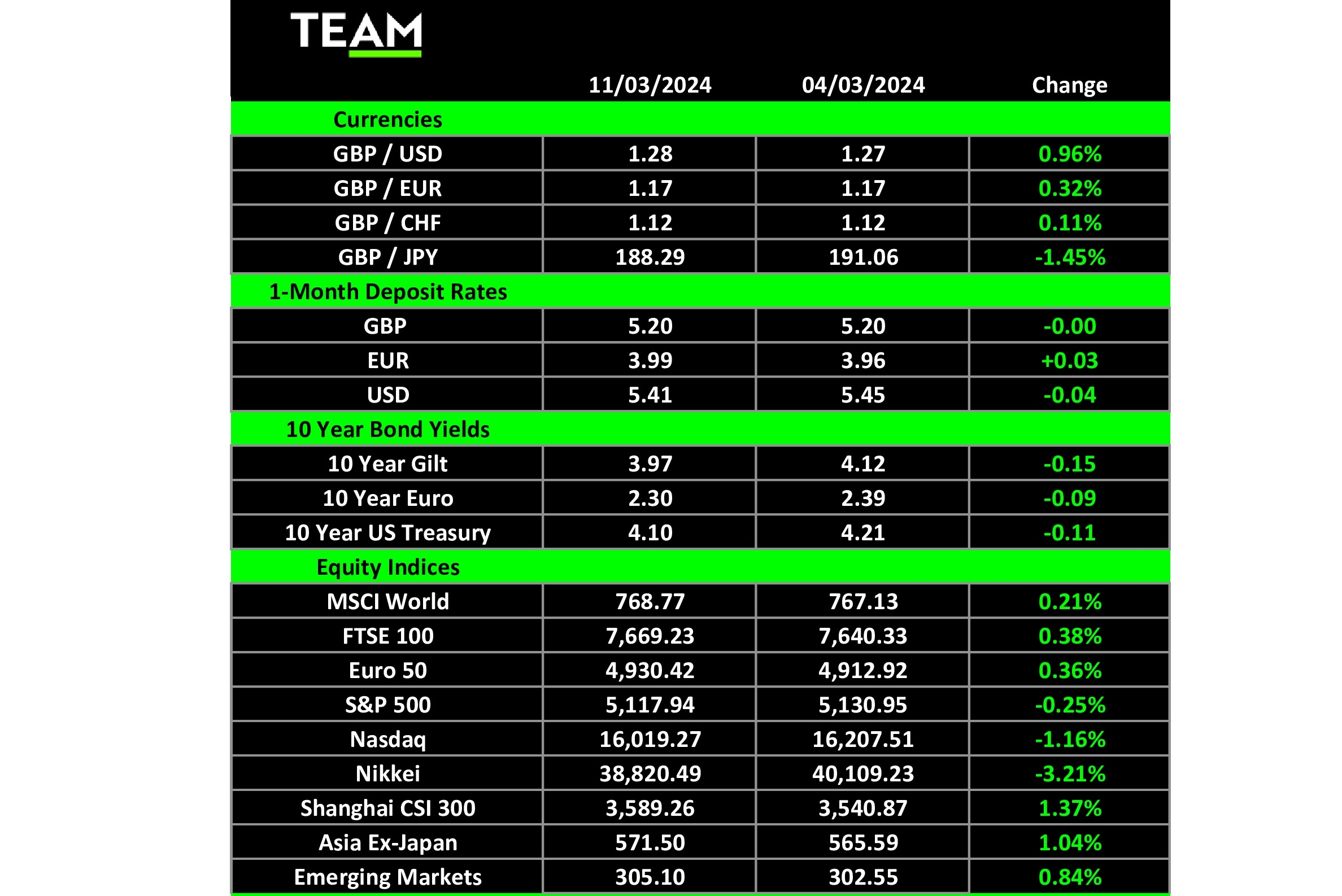

Sponsored Content

FOR months, artificial intelligence has powered North American stock markets upwards, but there are signs that momentum or enthusiasm is cooling as Nvidia, Broadcom and Intel all moved backwards last week.

A modest overall fall in American markets occurred, although there was interest in non-technology names which provided support.

The surprise was Continental Europe, which shone brightly as Christine Lagarde, the president of the European Central Bank, implied that June could be the earliest time that rates could be cut from the current 4% level. She predicted that inflation would reach its 2% target next year, but any help from the central bank could provide a fillip to activity levels, which is sorely needed. Growth is expected to be just 0.6% (0.8%) for 2024. We talk down the prospects of the UK, but clearly our domestic growth forecast of 0.9% is weak – but is still comfortably ahead of Europe.

Earlier in the week, Federal Reserve chair Jerome Powell mirrored the comments of Europe by saying it would be appropriate to reduce interest rates once it had gained greater confidence that inflation was moving sustainably toward 2%. Again, the implication is that inflation rates could start to move upwards temporarily, so a degree of caution is necessary as he does not wish to have to raise rates again after the first cut. The subsequent report of higher-than-expected job creation in the economy for February (275,000) verified the caution.

Joe Biden’s State of the Union address is being called “combative, fiery, feisty, strikingly political” and “argumentative” as the US President outlined the reasons that he deserves a second term. Hie two key themes were defending democracy (both domestically and abroad) and preserving reproductive rights. In terms of markets, the address had negligible impact on stocks or fixed-interest investments.

Politically, the speech was a positive for Biden, not because of anything he said, but for how he said it. For at least one evening, the President successfully pushed back against criticisms of his physical stamina and mental acuity. It also enabled his re-election campaign team to raise a record $10m in the following 24 hours after his performance.

America’s super-rich are cashing in some of their chips. Amazon founder Jeff Bezos sold shares valued at $8.5bn last month (Amazon shares have climbed 90% in the past year), while Mark Zuckerberg raised $638m from Meta (Facebook to you and me), which has climbed 180% in 12 months. Walmart’s Walton family sold shares valued at $1.5bn last week and another big-name seller included JPMorgan chief executive Jamie Dimon ($150m).

Is this the result of nervousness ahead of the November Presidential election? Or is it, simply put, that the S&P 500 index is up over 25% in the past year and is now at record highs? Whatever it is, it makes compelling sense to diversify and invest more broadly to avoid the problems of having all your eggs in one basket.

One of the international laggards for years has been China, but there was not good news last week when car sales were down 21% in February compared with 2023 and showed a 41% decline month on month. It would therefore be understandable to question whether the Chinese government’s prediction of a 5% growth rate in 2024 is realistic given the challenges the economy faces.

This coming week sees renewed inflation and factory gate price data in America and, on Friday, the Michigan Consumer Sentiment Survey is due to be released. All of these should be watched carefully, as they could disrupt the smooth sailing that world stock markets have experienced in the past few months.