Chancellor Rishi Sunak overshot the Government’s full-year borrowing target after the highest March figure for four years as Britain braces for ballooning public debt from mammoth coronavirus emergency measures.

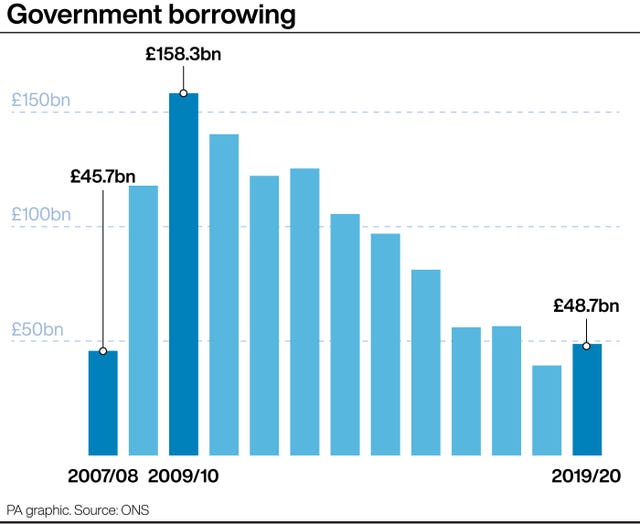

The Office for National Statistics (ONS) said public sector borrowing – excluding banks owned by the state – jumped £9.3 billion to a higher-than-forecast £48.7 billion in the financial year to March 31.

Borrowing surged to its highest March level since 2016 last month, at £3.1 billion – compared with an £891 million surplus a year earlier.

The March hike saw borrowing for the full year come in higher than the £47.4 billion forecast by the independent fiscal watchdog, the Office for Budget Responsibility (OBR).

It comes after the OBR last week said the budget deficit could soar by £218 billion this financial year to £273 billion, or 14% of gross domestic product (GDP) – the largest single-year deficit since the Second World War.

The ONS said: “The coronavirus (Covid-19) pandemic is expected to have a significant impact on the UK public sector finances.

“These effects will arise from both the introduction of public health measures and from new Government policies to support businesses and individuals.”

It added: “The full effects of Covid-19 on the public finances will become clearer in the coming months.”

The latest borrowing figures do not yet show the extra healthcare spending figures, while the Covid-19 support measures are not yet factored in as they were only launched in late March as Britain was placed in lockdown, while other policies did not come into effect until this month.

The ONS data showed debt – excluding state-controlled banks – rose to £1.8 trillion or 79.7% of GDP as at the end of March, up £30.5 billion on a year earlier.

The deficit stood at £3.05 billion alone in March.

Howard Archer, chief economist at the EY Item Club, said: “The public finances data for 2019/20 has been overtaken by recent events with the Government pledging significant fiscal support to businesses and household affected by coronavirus to help protect the economy as much as possible.

“Indeed, the EY Item Club suspects that the budget deficit will exceed £200 billion in 2020/21.”

But PwC chief economist John Hawksworth offered a glimmer of hope for the UK’s battered public finances.

He said: “Although the budget deficit this year could well be higher than the 10% of GDP peak seen after the global financial crisis, we would expect it to come down more rapidly to around 4%-7% of GDP in 2021/22 on the assumption the crisis has largely passed by then.

“This is because the temporary measures to support the economy through the lockdown would be able to be reversed and because the economy should recover gradually as and when the lockdown is eased.”