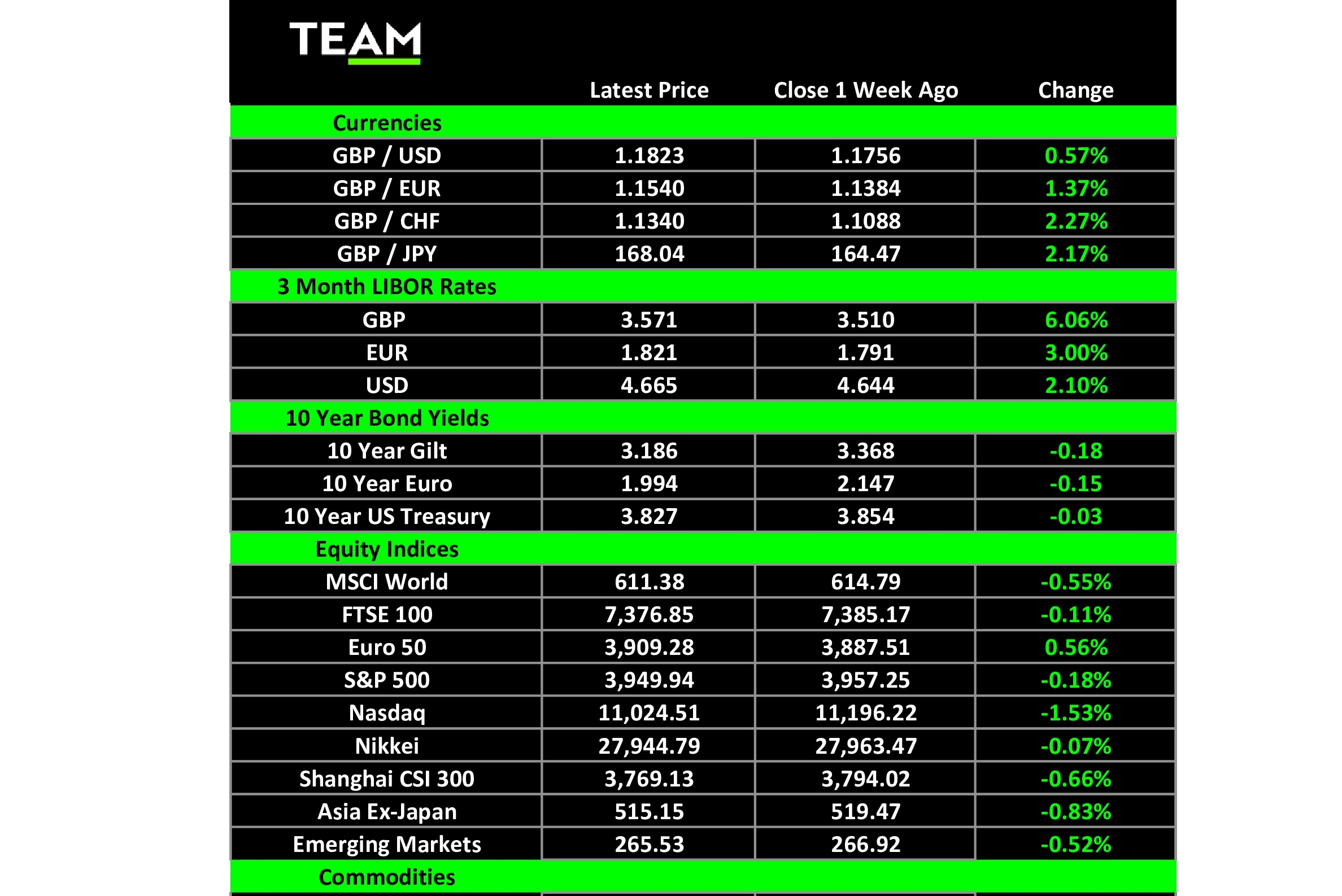

LAST week was a muddling one for stocks as the news flow and economic data gave conflicting signals. Another cooler inflation report, the US Producer Price Index, initially provided tailwinds for stocks but the rally faded as concerns over the health of the global economy was heightened by some of the biggest technology companies announcing plans to making sweeping job cuts. The blue-chip S&P 500 and technology-focused Nasdaq fell 0.2% and 1.5% respectively over the week.

Inflation has unnerved investors throughout this year but a second cooler-than-expected inflation report from the US in the space of just a few days offered more hope that price pressures are easing. On Tuesday it was reported that the US producers price index had risen just 0.2% between September and October, lower than the 0.4% consensus analyst forecasts, and the annual rate slowed to 8.0%.

This improving inflation outlook, however, has not reached this side of the Atlantic. A day later it was revealed that annual consumer price inflation in the UK had accelerated to 11.1% in October, the fastest pace since October 1981. The main upward pressure came from gas, electricity and food prices but it would have been a lot worse had the government not put in place the Energy Price Guarantee, capping the average annual household gas and electricity bill at £2,500.

Food prices rose 16.5% from a year earlier, the biggest increase in 45 years.

Bond markets reacted surprisingly well to the inflation report and the initial knee-jerk sell-off was soon reversed. Perhaps they were already focused on Jeremy Hunt’s budget to be unveiled the following day, much of which had already been leaked.

The tone of the chancellor’s autumn statement couldn’t have been more contrasting to that of his predecessor, which had triggered historic moves in UK government bonds and the pound at the end of September. He set out a return to fiscal orthodoxy, dubbed ‘Austerity 2.0’ by some, pledging to close a £55 billion deficit through a combination of higher taxes and lower spending in broadly equal measures. The 45p top rate of tax threshold was cut from £150,000 to £125,000 and the windfall tax on oil and gas companies operating in the North Sea was extended for a longer period at a higher rate.

This time around, the budget was also presented in tandem with an independent assessment from the Office for Budget Responsibility. Its outlook was stark, including a projection that real disposable household incomes would fall 4.3% in the current tax year, the biggest contraction since records began in 1956, and that the unemployment rate would climb to 4.9% through 2024.

The prospect of a prolonged recession and era of fiscal retrenchment is expected to ease the burden on the Bank of England to bring inflation back under control and money market futures are now pricing in UK interest rates peaking at 4.6% next autumn.

The US-listed American Depository Receipts of Taiwan Semiconductor Manufacturing jumped more than 10% on Tuesday after it was disclosed that Warren Buffett’s Berkshire Hathaway had built up a $4.1 billion stake in the chipmaker during the third quarter. TSMC is the leading manufacturer of the most advanced semiconductor chips used by phones, laptops and cars. It might seem surprising for the world’s most high-profile value investor to be investing in technology companies, the stake in TSMC sits alongside a near $130 billion holding of Apple and smaller investments in HP and Snowflake.

It was the turn of the traditional US bricks and mortar retailers to report third-quarter earnings and updates from Walmart, Home Depot and Lowe’s were all well received. Walmart shares gained 6.5% to a six-month high after it announced its revenues had been boosted by consumers switching to its lower-priced groceries.

Target, however, saw its shares fall by more than 15% after it warned ‘spending patterns changed dramatically’ in recent months and consumers are already cutting back discretionary purchases of clothing and housewares.

It was also a turbulent week for energy and the price of brent crude fell $6 to $87 a barrel as markets weighed the outlook for demand against the increased risk of recession and doubts over speculated relaxations of China’s zero-Covid policy. Over the weekend, the world’s largest importer of crude oil announced its first fatalities from Covid since May and Guangzhou, home to nearly 19 million people, imposed a five-day lockdown on its most populous district of Baiyun.