THE run of three consecutive weekly gains came to an abrupt halt last week after the US Federal Reserve warned that interest rates could go higher than markets expect as it strives to bring down inflation.

Team Asset Management offer their weekly round-up of global markets

Sponsored Content

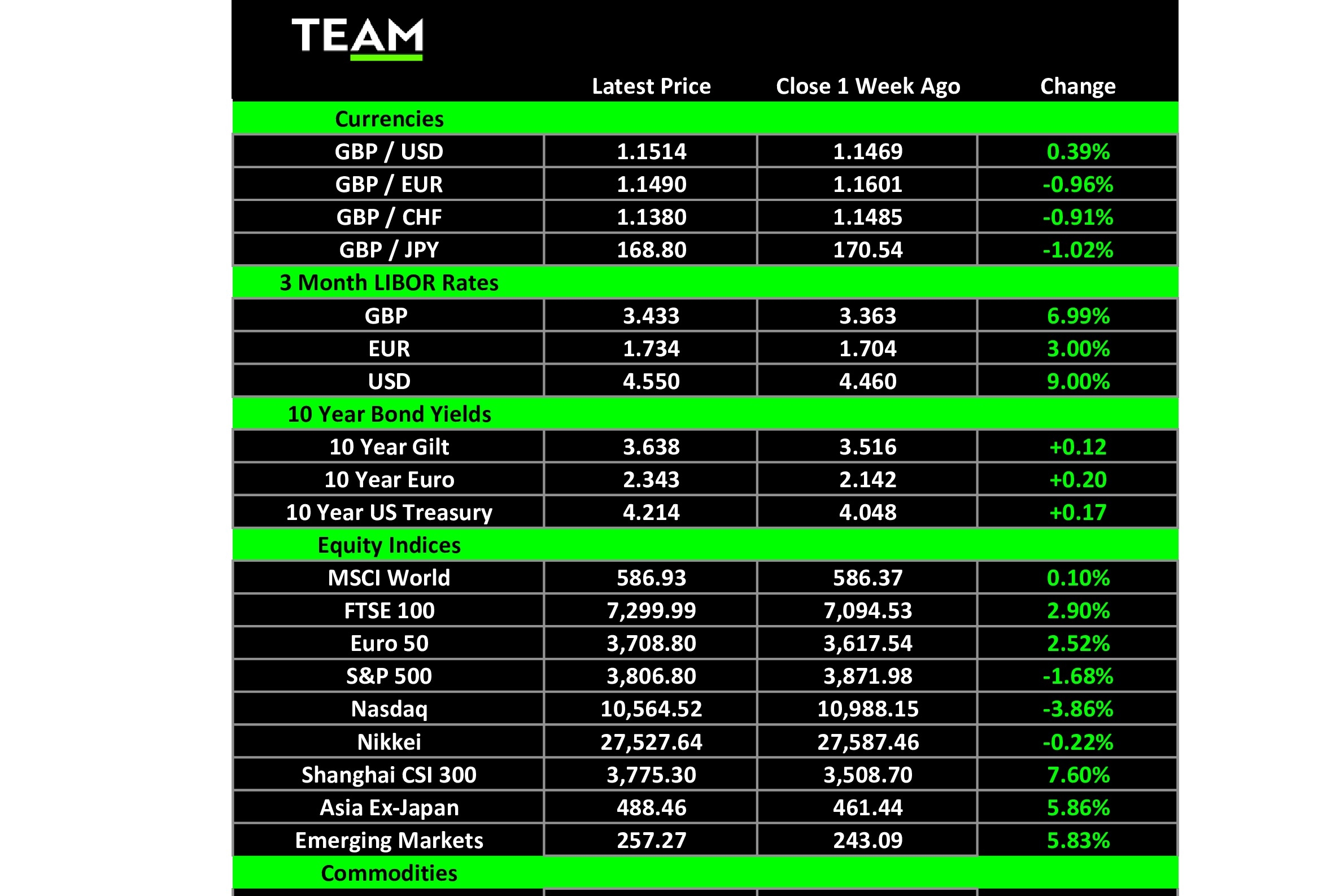

The blue-chip S&P 500 fell 1.7% and the technology-focused Nasdaq, which is more sensitive to changes in long-term interest rates, 3.9%. The FTSE 100, however, benefited from its higher exposure to energy and materials stocks and gained 2.9%.

Markets fully expected the Federal Reserve to hike its benchmark rate on Wednesday by 0.75% for the fourth time in a row, but the hawkish tone of the subsequent press conference caught many investors off-guard. Chairman Jay Powell warned the Fed still had ‘some ways to go’ to get inflation under control and recent data suggested interest rates would have to move higher than previously thought.

While Powell conceded that it took time for higher interest rates to have an impact on inflation and economic activity, he made it clear that a series of moderating monthly inflation reports were needed for the Fed to ease off. His comments sent US mortgage rates, which had recently moved above 7% for the first time in 20 years, even higher.

The Bank of England’s Monetary Policy Committee met the following day and, as expected, raised its benchmark interest rate by 0.75%. However, the decision wasn’t unanimous as two out of the nine members voted for more modest increases of 0.25% and 0.5%. The split within the committee reflects the more challenging economic outlook faced by the UK and Europe, compared to the US. Dependence on imported energy has amplified inflationary pressures and both the Bank of England and European Central Bank are hiking interest rates at the cost of prolonging inevitable recessions.

October’s monthly nonfarm payrolls report provided more evidence that the US economy is in a better position to withstand higher interest rates. It revealed that 261,000 more positions across the economy had been added, better than the consensus analyst forecasts of 200,000.

It was another difficult week for technology companies, but not just because of the prospect of even higher interest rates. Elon Musk announced he would cut Twitter’s 7,500 workforce by half to reduce losses of more than $4m a day. Since he acquired Twitter, which is now delisted from the New York Stock Exchange, companies including Carlsberg, General Motors, L’Oréal and Volkswagen have suspended advertising on the social-media platform owing to concerns over content moderation.

In contrast, airlines enjoyed a good week. EasyJet shares gained more than 8% following speculation it could become a target for one of Europe’s larger airline groups, such as British Airways’ parent IAG, or Air France-KLM. The lossmaking budget airline has cut its winter schedule and its shares trade some 75% lower than at the start of the pandemic.

Rival low-cost airline Ryanair has fared much better and reported a pre-tax profit of 1.4 billion euros for the six months to 30 September. In the same period a year ago, it lost 100 million euros. Chief executive Michael O’Leary also revealed that Europe’s largest budget airline was ‘seeing very strong forward bookings’.

Chinese stocks were also standout performers last week amid speculation that authorities in Beijing are preparing to relax Covid restrictions. The Shanghai CSI 300 and Hong Kong’s Hang Seng Indices rose 7.6% and 13.0% respectively. The markets have mostly held on to the gains despite the country’s National Health Commission reiterating its commitment to eliminating Covid-19 over the weekend.

The optimism over China also boosted energy prices last week with Brent crude jumping $3 to $98 a barrel. China is the world’s largest importer of oil, and any gradual return to normalisation of economic activity in the country would have a meaningful impact on demand-supply dynamics.